As Dubai’s real estate market matures, a new chapter is unfolding — one defined by stability, end-user depth, and long-term value creation rather than speculative turnover. After nearly a decade of vertical expansion dominated by apartment towers and high-density urban projects, investor attention is now shifting decisively toward low-density, land-anchored assets — specifically townhouses and villas.

Between 2021 and 2024, Dubai’s residential market experienced an extraordinary run. Apartments accounted for more than two-thirds of total transactions, fuelled by a wave of post-pandemic relocations, global capital inflows, and the city’s ambitious off-plan development pipeline. Prices surged as investors chased short-term capital gains, and many communities saw record absorption rates. Yet, as 2025 begins, the underlying dynamics are changing. The rapid escalation of supply in the apartment segment, coupled with rising construction costs and moderating yields, has prompted both institutional and private investors to reassess where sustainable value truly lies.

At the same time, Dubai’s demographic and regulatory evolution is reshaping demand. The introduction of long-term residency visas, flexible company ownership laws, and the continued influx of high-skilled professionals have deepened the city’s end-user base. These new residents are not transient buyers looking for short-term rental arbitrage — they are families, entrepreneurs, and executives building permanent roots in the emirate. Their priorities are markedly different: more space, privacy, outdoor areas, and community-based living — features that villas and townhouses naturally provide.

In parallel, developers are re-orienting their product strategies toward horizontal master-planned communities. Projects such as Emaar’s The Valley, Majid Al Futtaim’s Tilal Al Ghaf, and Damac’s Lagoons illustrate this trend — offering integrated schools, retail, parks, and sustainable designs in low-rise environments. These developments reflect the global post-pandemic lifestyle shift: a preference for open space and quality of life over compact urban density.

From an investment standpoint, these shifts have measurable outcomes. Market data from JLL, CBRE, and ValuStrat shows that villas outperformed apartments in both price growth (+72% vs +45% since 2021) and rental stability, while also experiencing lower vacancy rates and longer tenant retention periods. Furthermore, their limited pipeline — less than 15% of total upcoming residential deliveries — makes them structurally scarce in a city where demand continues to expand.

In essence, Dubai is moving from a “build-to-boom” to a “build-to-sustain” era. The skyline that once symbolized growth through vertical ambition is now complemented by the spread of modern, community-centric villa enclaves that represent enduring value and lifestyle permanence.

For new investors entering the market in 2025–2026, understanding this transformation is crucial. The metrics that once favored apartments — faster liquidity, lower entry costs, and shorter holding periods — are giving way to a new calculus centered on risk-adjusted stability, yield durability, and tangible land ownership.

This report explores in depth why townhouses and villas are emerging as the most strategic property segment in Dubai’s maturing real estate landscape — combining capital resilience, lifestyle alignment, and long-term wealth creation potential.

1. Limited Supply and the Growing Scarcity Premium

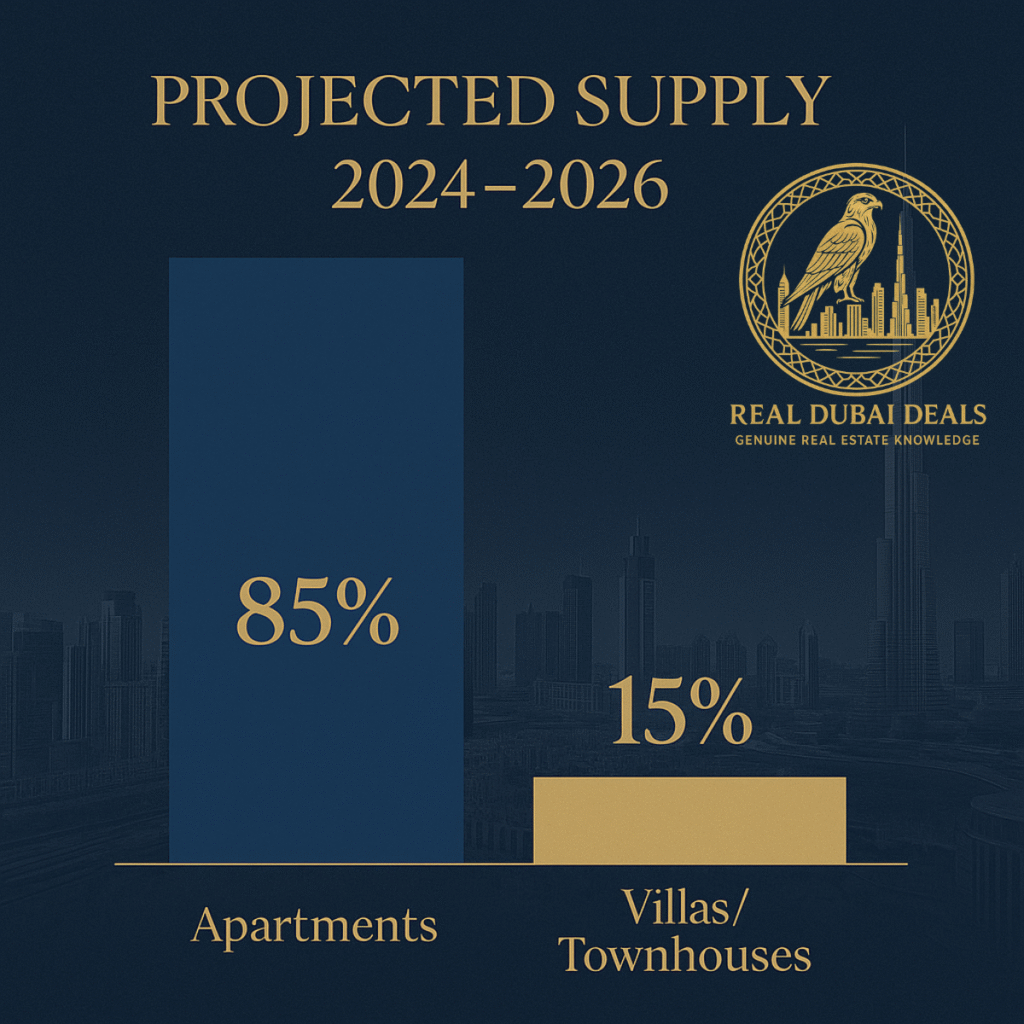

Despite record construction activity across Dubai, the composition of the city’s development pipeline reveals a significant imbalance — one that strongly favors investors in townhouses and villas over the medium term. According to the latest data from JLL and CBRE, Dubai is projected to deliver around 66,000 new residential units in 2025, followed by more than 70,000 additional completions in 2026. Yet, fewer than 15% of these upcoming deliveries are in the villa and townhouse segment — a share that has remained largely unchanged for the past five years.

Vertical Supply, Horizontal Scarcity

The overwhelming majority of upcoming projects — more than 85% of all new units — continue to be concentrated in high-density apartment developments, particularly in areas such as Business Bay, JVC, Dubai Creek Harbour, and Downtown. Developers favor these vertical formats for efficiency: apartment towers allow higher returns on smaller land plots, faster permitting cycles, and easier phasing for cash flow management.

However, this bias toward high-rise housing has created a persistent under-supply in low-density, family-oriented properties. Even as the overall number of units increases, the portion of available townhouses and villas remains stagnant, resulting in a structural shortage of horizontal living options.

The contrast is stark: while new apartment clusters rise across the city’s skyline, communities offering private gardens, larger layouts, and outdoor space are reaching capacity saturation. Neighborhoods like Arabian Ranches, The Lakes, Meadows, and Palm Jumeirah are nearly built out, leaving limited scope for new villa inventory within established zones.

Emerging villa projects — The Valley, Tilal Al Ghaf, Sobha Hartland 2, and Emaar South — are therefore absorbing extraordinary demand. Many of these communities report full or near-full reservation of off-plan inventory well before handover, highlighting the unmet appetite for land-based housing.

The Economics of Scarcity

Scarcity in real estate is not a temporary imbalance; it is a long-term value catalyst. When a specific asset class has constrained supply, its value resilience is amplified during downturns and its recovery speed accelerates once confidence returns. Historical data from ValuStrat and REIDIN demonstrates this pattern clearly:

- During the 2015–2019 correction, villa prices in Dubai fell by approximately 12%, while apartment prices dropped by over 25%.

- In the subsequent 2021–2024 recovery, villa prices surged by 70%, outpacing apartment growth by nearly 30 percentage points.

This differential is not driven by speculation but by livability-based demand. Families and long-term residents tend to prioritize villas for space, privacy, and community amenities — factors that sustain value regardless of short-term market sentiment.

Population Growth and Structural Undersupply

Dubai’s population, now exceeding 3.7 million, is projected to reach 5.8 million by 2040, according to the Dubai Urban Master Plan. As this demographic base expands, the gap between available housing types will widen. Most new residents entering the ownership market over the next decade will demand family-scale housing rather than transient apartment living.

Yet, the pipeline composition does not reflect this future need. The proportion of villa deliveries remains capped by land availability and development cost, ensuring a built-in scarcity premium for existing and upcoming townhouse communities.

Investor Implications

For investors, this supply imbalance translates into several tangible advantages:

- Capital Resilience: With limited new stock, villa prices are less susceptible to overbuilding cycles that frequently affect apartment districts.

- Faster Absorption: Low supply coupled with genuine end-user demand ensures quick take-up of new villa launches and resales.

- Price Stickiness: Villas experience shallower corrections during market downturns, preserving long-term capital value.

- Rental Leverage: The shortage of family-sized properties sustains strong lease demand, particularly from expatriates on long-term visas seeking quality homes.

In effect, the Dubai market has entered a phase where quantity and quality have diverged. The quantity of apartments continues to rise, but the quality of investment opportunities increasingly resides in the villa and townhouse sector — where scarcity is structural, not cyclical.

Investor Insight

For new entrants to the market, the lesson is clear:

Invest where supply cannot catch up.

The limited pipeline of horizontal homes, combined with Dubai’s growing base of end-user residents, ensures that villas and townhouses will remain the city’s most defensive and appreciating asset class throughout the 2025–2030 horizon.

Would you like me to now design an infographic or data visualization panel to accompany this section — for example,

“Dubai Housing Pipeline 2024–2026: Vertical vs Horizontal Supply”,

featuring a skyline silhouette, 85% apartments vs 15% villas, and a gold-blue contrast in your OSAC Properties theme?

End-User Driven Demand and Mortgage Accessibility: The New Foundation of Market Stability

Over the past few years, Dubai’s real estate landscape has undergone a fundamental transformation in its buyer demographics. The villa and townhouse segment, once the domain of short-term investors and speculative flippers, is now increasingly being shaped by end-user families and long-term residents. This shift represents one of the most significant structural changes in the market since 2012 and has redefined both demand quality and price behavior.

A Shift from Speculation to Occupation

Historically, much of Dubai’s residential demand was cyclical and speculative. Buyers often entered off-plan projects to capitalize on early launch premiums, selling before completion to realize quick gains. However, from 2022 onward, a marked transition toward genuine end-user ownership has taken hold — driven by a combination of policy, affordability, and lifestyle evolution.

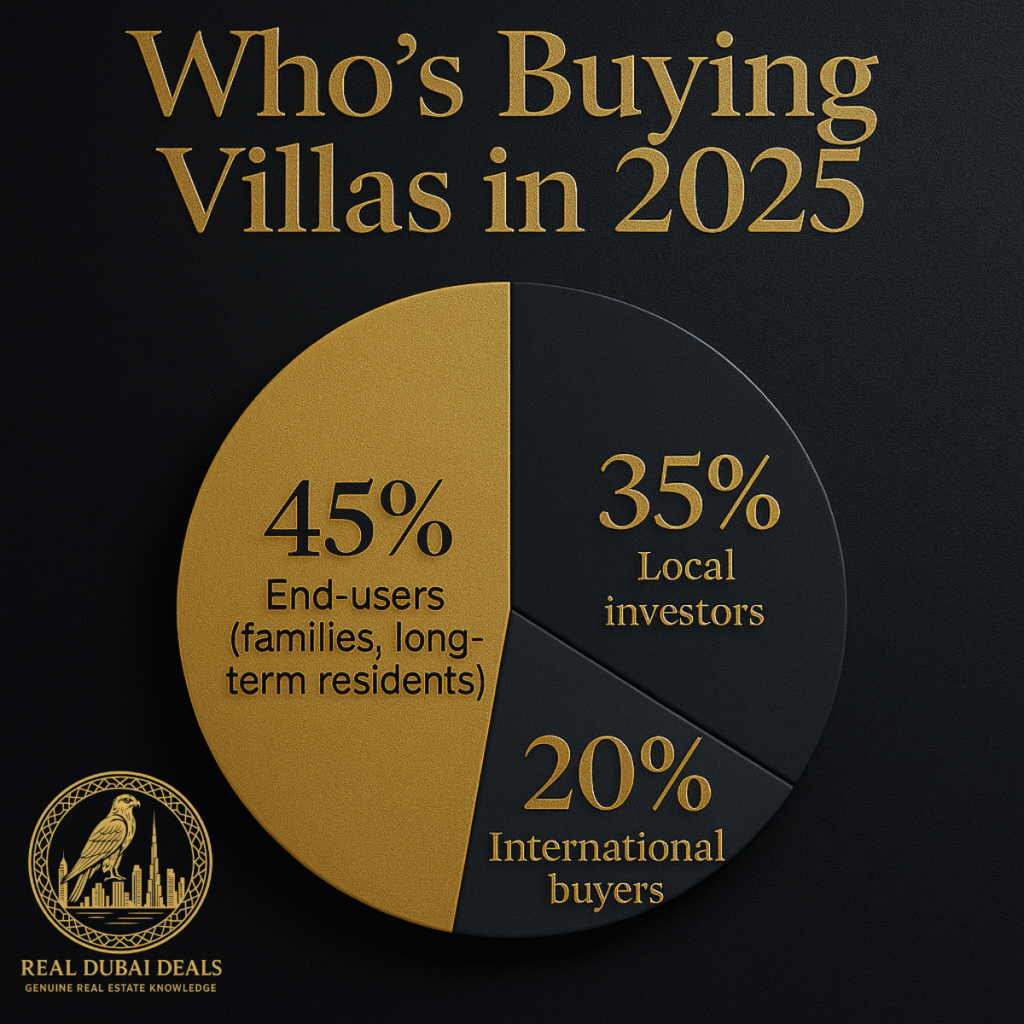

According to data from CBRE and ValuStrat, nearly half of villa purchases in 2025 are now end-user driven, compared with less than 30% just five years ago. This surge is largely fueled by expatriates who now view Dubai as a permanent home rather than a temporary post. Many are high-earning professionals, entrepreneurs, and retirees who have benefited from government reforms granting multi-year residency rights, business ownership privileges, and long-term visas linked to property investment.

The Role of Residency Reforms

Dubai’s Golden Visa, Green Visa, and Retirement Visa programs have transformed the buyer profile.

- The Golden Visa (10-year residency) grants property owners long-term stability and eliminates previous constraints around renewals and sponsorship.

- The Green Visa caters to skilled professionals and freelancers, encouraging younger expatriates to settle with families.

- The Retirement Visa allows older investors to downsize or relocate to Dubai permanently, further strengthening demand in villa communities.

These reforms have effectively anchored expatriate wealth within Dubai’s economy, turning transient renters into committed homeowners. The result is a more stable, less speculative property market, particularly across suburban villa zones such as Arabian Ranches, Mudon, The Valley, Tilal Al Ghaf, and Dubai Hills Estate.

Lifestyle Preferences: The Pull of Space and Privacy

The appeal of villas and townhouses is not purely financial — it is deeply rooted in lifestyle preferences.

Modern residents increasingly prioritize:

- Private outdoor space for family activities and wellness.

- Larger interiors conducive to hybrid work lifestyles.

- Secure gated communities with green areas, schools, clinics, and retail amenities.

These attributes reflect a global post-pandemic trend: the pursuit of “livable luxury” — properties that blend comfort, accessibility, and long-term functionality. Villas cater perfectly to this demand, offering something apartments rarely can: a sense of permanence and individuality.

Easing EIBOR and Improved Mortgage Accessibility

Affordability, long considered a constraint for end-user buyers, is gradually improving. The Emirates Interbank Offered Rate (EIBOR) — the benchmark for local mortgage pricing — has begun to ease, falling from 5.3% in early 2025 to approximately 4.8% in Q3. This modest reduction has tangible effects on borrowing capacity.

Every 1% decrease in mortgage rates translates to roughly 10–12% improvement in affordability, allowing more end-users to transition from renting to ownership. Simultaneously, banks have begun offering longer-term fixed-rate mortgages (up to 25 years), with more flexible repayment options and lower down payment requirements for salaried residents.

Developers are also responding strategically: several major firms now provide 80–90% post-handover payment plans, spreading costs across 3–5 years after delivery. These structures bridge the affordability gap between aspirational tenants and new homeowners, unlocking a larger pool of buyers in the mid-income segment.

Sustainability and Stability in Returns

Unlike investor-driven cycles, where rapid buy-and-sell behavior amplifies volatility, end-user-driven demand is inherently more durable and predictable.

Families purchasing villas tend to hold for extended periods — typically 8–12 years — either as a primary residence or as part of a long-term wealth plan. This behavior creates a more balanced and self-sustaining market, reducing the amplitude of price fluctuations and maintaining rental stability.

For investors, this evolution offers two clear benefits:

- Occupancy stability — tenants transitioning into owners open rental opportunities in the mid-tier segment while preserving rental rates in prime communities.

- Yield sustainability — consistent end-user absorption keeps prices supported even during broader market slowdowns.

Investor Insight

End-user demand now acts as the market’s shock absorber, providing continuity in cash flow and price resilience. Unlike speculative booms that end abruptly, this new phase of organic growth ensures steady long-term returns.

In essence, the Dubai villa market has entered an era where homeownership replaces speculation, and where mortgage accessibility and lifestyle quality drive genuine demand. For investors entering in 2025–2026, this dynamic represents not just a safer entry point — but a strategic opportunity to align with the most stable force in Dubai’s real estate cycle: the end-user family.

3. Capital Appreciation Performance: Where Land Outperforms Concrete

Over the past four years, Dubai’s property market has offered a clear lesson in capital growth dynamics: land-based assets outperform vertical assets.

According to ValuStrat’s Price Index (VPI) and corroborated by CBRE and Knight Frank, the villa segment has delivered approximately 72% capital appreciation between 2021 and 2025, compared with 45% growth across apartments. This divergence is more than statistical — it reflects the long-term economics of scarcity, ownership control, and lifestyle demand that favor horizontal living.

Why Villas Outperform Apartments

At the most fundamental level, villas are tied to finite land, while apartments represent a share of built-up space that can be easily replicated. As developers continue to launch high-rise towers across Dubai’s urban core, the supply of true land-backed property — independent or semi-detached homes — remains constrained. This scarcity is magnified by zoning limits in established districts such as Arabian Ranches, The Lakes, Palm Jumeirah, and Emirates Hills, where future expansion potential is minimal.

In contrast, apartment supply is both scalable and cyclical. Developers can launch new towers at short notice in high-demand corridors, making apartment prices more sensitive to market sentiment and construction activity. Villas, by design, are inherently non-replicable assets, and this fundamental difference underpins their superior capital performance.

Performance Across Market Cycles

The resilience of villa pricing is not just a feature of boom cycles; it extends across downturns. Historical market data confirms this consistency:

- During the 2018–2020 correction, villa prices declined only 10%, while apartment values fell 22%, underscoring the segment’s defensive nature.

- When the market entered its post-pandemic recovery, villas led the rebound, gaining more than 70% in value from 2021 to 2025, compared with a 45% rebound in apartments.

This pattern demonstrates that villas not only recover faster but also retain value through volatility, making them the asset class of choice for long-term investors seeking both growth and protection.

Community-Level Appreciation

The strongest villa price appreciation has been concentrated in well-planned, amenity-rich master communities that combine accessibility, lifestyle infrastructure, and strong developer branding.

Notable examples include:

- Dubai Hills Estate: Rapid development of schools, parks, and retail zones transformed the area into a top-performing submarket, with villas appreciating over 65% since 2021.

- Palm Jumeirah: As Dubai’s global luxury address, villa values surged more than 80%, driven by scarcity, prime land, and international prestige.

- Arabian Ranches & The Meadows: Mature, family-centric enclaves saw steady double-digit growth with minimal vacancy, favored by long-term expatriates seeking community living.

Emerging master plans like Tilal Al Ghaf and Sobha Hartland 2 are replicating this success formula — combining architectural quality with lifestyle-oriented amenities that enhance both livability and resale value.

Investor Psychology and Market Maturity

Another factor fueling villa outperformance is the evolution of buyer psychology.

In earlier cycles, investors favored apartments for liquidity and entry affordability. But today’s buyers — particularly end-users and high-net-worth individuals — prioritize quality of life, permanence, and exclusivity. Villas and townhouses, with private gardens, limited density, and premium community settings, fulfill these aspirations.

This demand is further reinforced by the rise in high-net-worth migration to Dubai. Data from Henley & Partners indicates that more than 4,500 millionaires relocated to the UAE in 2023–2024, a portion of whom targeted prime villa districts. Such inflows anchor price growth at the upper end of the market and stabilize demand even during macroeconomic fluctuations.

Economic Foundations of Appreciation

The capital performance of villas also correlates with macroeconomic strength. Dubai’s continued expansion in trade, tourism, technology, and finance has driven job creation, population inflows, and purchasing power — all feeding housing demand. Yet, because apartment supply expands proportionally while villa construction remains restricted by land, the price elasticity of villas remains steeper, meaning even modest increases in demand translate to outsized appreciation.

This supply-demand asymmetry explains why villa values not only outperform during upcycles but also maintain long-term compounded growth. For example, the compound annual growth rate (CAGR) for villas between 2021 and 2025 stands at roughly 14.5%, compared with 9.5% for apartments.

Investor Implications

From an investor perspective, villas deliver a powerful risk-return profile:

- Downside Protection: In cyclical corrections, villas decline less due to constrained supply and stronger end-user anchoring.

- Upside Amplification: In recovery phases, pent-up demand and limited inventory drive faster appreciation.

- Liquidity Resilience: High demand for ready villas ensures quicker resale times, especially in established communities.

- Portfolio Diversification: Holding villa assets balances the volatility of high-rise properties, providing a stabilizing anchor for real estate portfolios.

Investor Insight

Villas are not just homes — they are land-based equity instruments that combine tangible ownership with long-term appreciation potential. They serve both as lifestyle assets and as strategic financial hedges against inflation and market cycles.

In Dubai’s evolving real estate landscape, this dual advantage — downside protection and amplified upside — positions villas and townhouses as the city’s most durable path to sustained capital growth through 2030 and beyond.

4. Rental Yields and Net Return Efficiency: Where Quality Now Outperforms Density

For many years, Dubai’s apartment market was the clear frontrunner in terms of rental yield, driven by lower entry prices, rapid turnover, and investor-friendly liquidity. However, as the market matures, that historical advantage is gradually eroding. The city’s rental landscape is now defined by a shift in tenant preference — away from compact, high-rise living toward spacious, family-oriented homes in horizontal communities.

This shift is reshaping the economics of return on investment. Today, townhouses and villas are narrowing — and in some cases surpassing — the yield gap once dominated by apartments, especially when factoring in net return efficiency after service charges and maintenance costs.

Tenant Migration and Demand Redistribution

Over the past two years, Dubai has witnessed a steady migration of tenants from apartments to suburban villa communities, driven by lifestyle upgrades, family formation, and affordability stabilization. Popular developments such as Damac Lagoons, Dubailand, Mudon, and Serena have benefited most from this movement.

These communities offer larger spaces, private gardens, and secure environments at rents that remain competitive relative to smaller urban apartments. As a result, occupancy levels in townhouse clusters are near all-time highs, and landlords in these segments now enjoy waiting lists of prospective tenants.

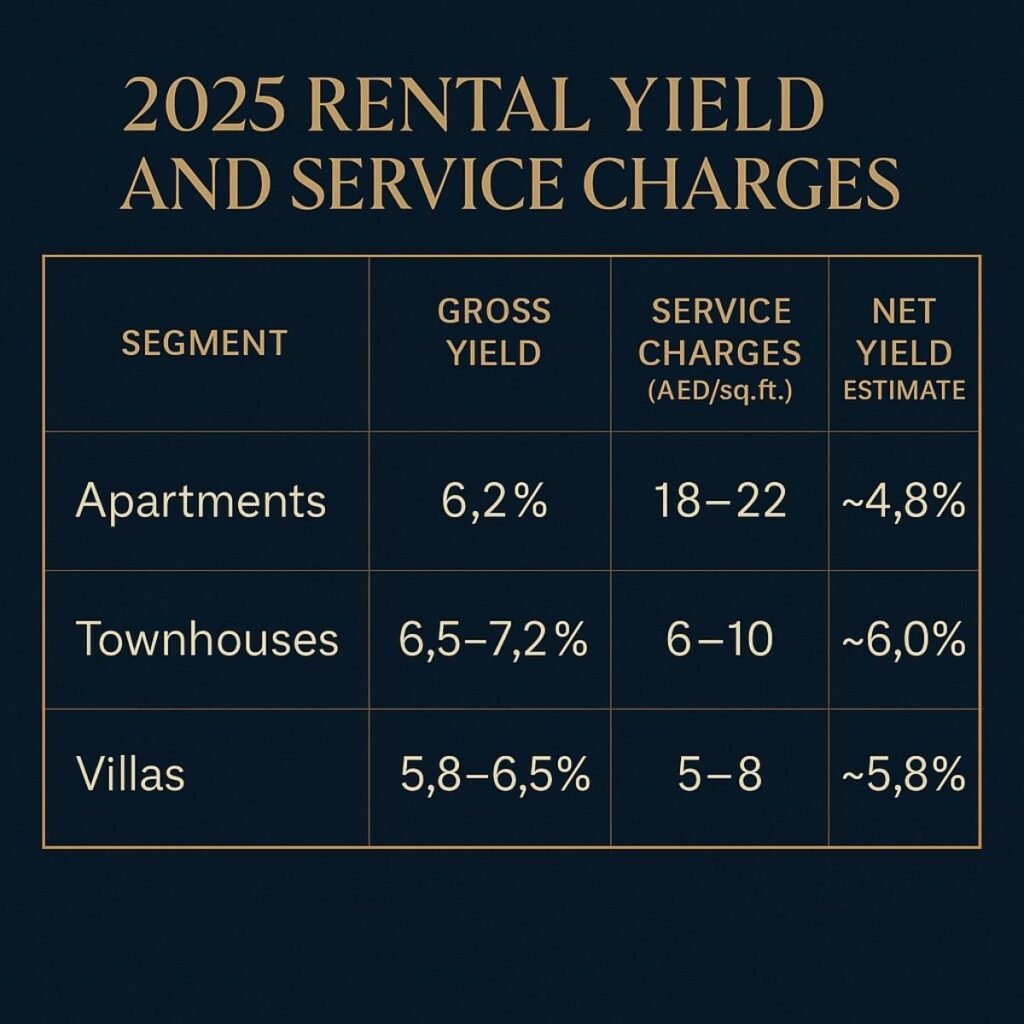

Data from CBRE and ValuStrat show that average townhouse rents have risen by 18–22% annually since 2023, outpacing the broader market average. This surge has effectively lifted gross yields for mid-tier townhouses to 6.5–7%, placing them at par — and in some cases above — apartment yields in central districts.

Meanwhile, premium villas in master communities such as Dubai Hills Estate, Arabian Ranches, and The Meadows are achieving gross yields between 5.8% and 6.5%, a remarkable figure for the luxury segment, which traditionally traded lower yields in exchange for capital appreciation.

Service Charges and Maintenance: The Hidden Yield Killer

While gross yield is an important indicator, it often hides the real story of profitability. The key differentiator in 2025 is net yield efficiency — the actual return after operating costs, association fees, and maintenance charges.

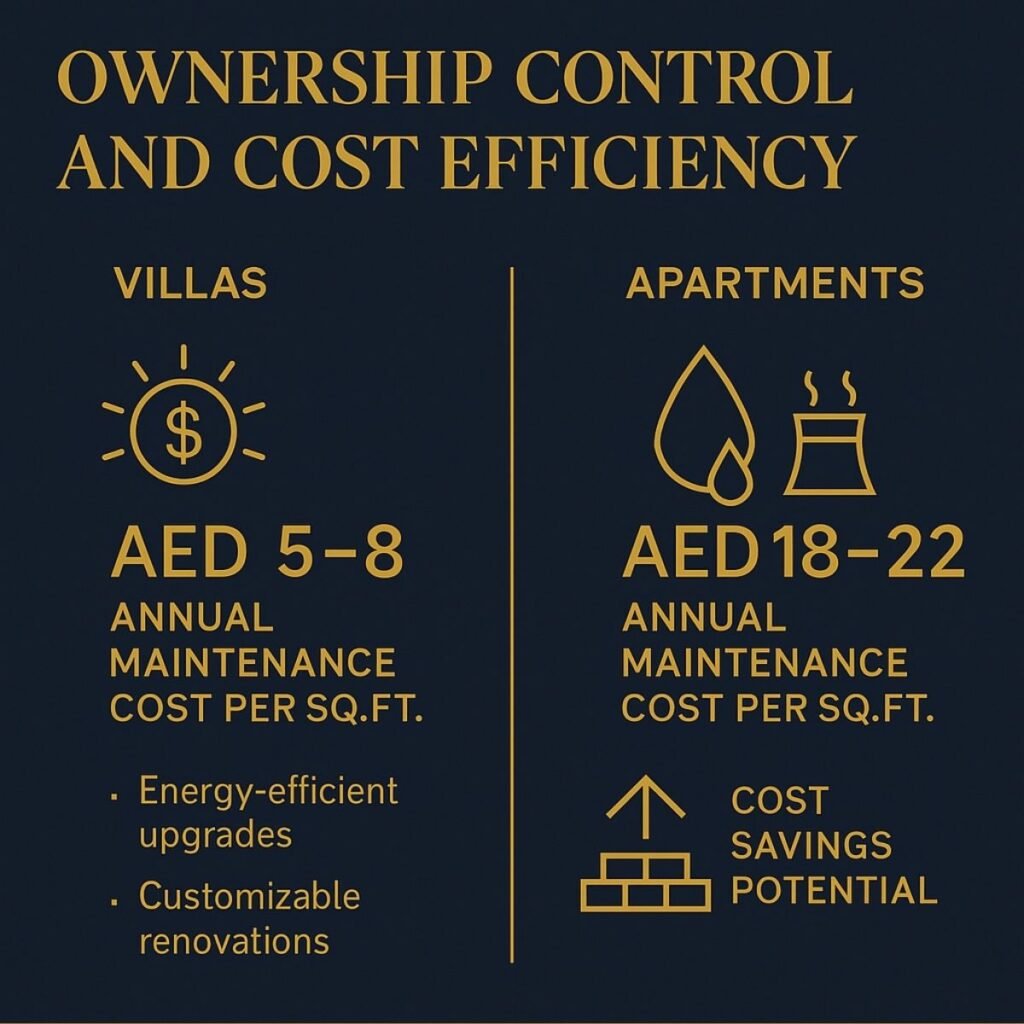

In high-rise apartments, service charges range between AED 18–22 per sq. ft. annually, primarily covering building management, cooling systems, elevators, and façade upkeep. These expenses can erode up to 25–30% of the investor’s gross income, especially in older or high-maintenance buildings.

By contrast, villas and townhouses carry much lower annual outgoings — typically between AED 5–10 per sq. ft. With fewer shared facilities and simpler mechanical infrastructure, owners can directly manage maintenance schedules and cost structures.

This means that while apartment yields may appear comparable at first glance, their net profitability is often inferior once these recurring charges are accounted for. In practice, many investors discover that a villa generating a 6% gross yield can outperform an apartment showing 6.5% on paper — simply due to lower expenses and better control over property management.

Stability and Retention: Yield Beyond Numbers

Another hidden driver of yield efficiency is tenant stability. Families renting villas and townhouses tend to stay longer, typically extending leases for multiple years. This reduces turnover costs such as repainting, marketing, and brokerage commissions, which can significantly cut into returns for apartment landlords who face annual churn.

Longer tenancies also mean fewer vacancy gaps — a crucial factor in preserving yield consistency. According to CBRE’s Q2 2025 data, average tenancy duration in villa communities now exceeds 3.5 years, compared with 1.8 years in apartment clusters.

This stability translates directly into higher effective net income, reinforcing villas’ advantage as long-term income-producing assets.

Yield Gradient Across Segments

The modern yield structure of Dubai’s residential market illustrates a compression between apartments and villas, once separated by several percentage points:

This table shows that when adjusted for real operating costs, villas and townhouses now rival or outperform apartment investments on a net basis. The higher stability, lower maintenance burden, and longer occupancy durations compound these advantages over time.

Investor Insight

Investors often focus on nominal yields but overlook the efficiency of income. Dubai’s maturing market rewards assets that balance operational simplicity with stable occupancy — and this is where villas and townhouses excel.

- Net yield supremacy: Once service charges and maintenance are considered, villas can deliver 15–20% higher real income than apartments.

- Operational control: Villa owners manage their costs independently, rather than relying on association-managed budgets.

- Tenant retention: Long-term family occupancies reduce annual expenses and protect revenue consistency.

In essence, the profitability hierarchy in Dubai real estate is shifting. Apartments may still offer liquidity and lower entry costs, but villas and townhouses now provide superior efficiency, resilience, and total return — a critical distinction for investors navigating the next phase of Dubai’s property cycle.

5. Maintenance Savings and Customization Control: Unlocking True Net Return Potential

In Dubai’s maturing property market, one of the most underestimated yet decisive advantages of investing in villas and townhouses over apartments lies in operating cost efficiency and customization flexibility.

Where apartment owners often contend with collective service fees, shared maintenance liabilities, and rigid building regulations, villa investors benefit from financial control, cost transparency, and the ability to enhance value through strategic improvements.

The Weight of Shared Costs in Apartments

Apartment ownership, while convenient, comes with unavoidable collective obligations. Building management companies levy annual service charges to cover a wide array of shared expenses:

- Air-conditioning and chiller systems

- Elevator maintenance and emergency servicing

- Security and cleaning of common areas

- Façade repairs, lighting, and parking upkeep

In premium apartment towers, particularly in Downtown Dubai, Business Bay, and JLT, these costs can easily exceed AED 18–22 per sq. ft per year, consuming up to 25–30% of an investor’s gross rental income.

Furthermore, apartment owners have little to no control over how funds are spent. Decisions on maintenance schedules, vendor selection, or budget allocation are handled by owners’ associations and management firms, where individual owners have limited influence.

This centralized structure may ensure uniform upkeep, but it also locks investors into a fixed cost environment that doesn’t adapt to market conditions. Whether occupancy rates are 60% or 100%, the fees remain constant, impacting yield during slower rental cycles.

Villas: A Model of Financial Autonomy

Villa ownership reverses this dynamic completely. Since villas are independent or semi-independent properties, owners directly manage their maintenance decisions. This autonomy allows for cost optimization, customized scheduling, and efficiency-driven improvements.

Typical maintenance costs for villas range from AED 5–8 per sq. ft annually, less than half the cost of high-rise apartments. Moreover, expenses can be tailored: an owner can choose when to service HVAC systems, select their preferred contractors, or implement upgrades that generate long-term savings — such as:

- Solar panel installations to offset electricity bills.

- Energy-efficient lighting and insulation to reduce cooling expenses.

- Smart irrigation systems for gardens to minimize water use.

These owner-led improvements not only reduce running costs but also elevate the property’s market appeal, positioning it competitively for both resale and rental purposes.

Customizability and Value Creation

Perhaps the most powerful differentiator is the freedom to modify and personalize. Apartment owners are bound by uniform layouts and design restrictions, but villa investors can enhance living space through extensions, interior redesigns, or amenity upgrades such as:

- Adding private pools, pergolas, or landscaped decks.

- Upgrading interiors with smart-home automation or contemporary finishes.

- Expanding built-up areas (subject to community guidelines).

These customizations often yield rental premiums of 10–20% compared to unmodified units in the same community. Unlike apartment improvements that primarily benefit tenants, villa upgrades translate directly into asset appreciation, ensuring tangible returns on renovation investment.

In communities like The Meadows, Arabian Ranches, and Jumeirah Park, upgraded villas routinely command AED 400,000–600,000 higher resale values than standard counterparts — clear evidence of how customization translates to capital gain.

Operational Flexibility and Resale Leverage

Operational independence also enhances resale flexibility. Villa owners can stage, renovate, or reposition their property before listing, ensuring maximum visual and functional appeal. Apartments, constrained by building-wide uniformity and shared maintenance conditions, rarely allow such pre-sale optimization.

In an increasingly design-conscious market where buyers prioritize aesthetics, layout efficiency, and energy savings, the ability to control and enhance one’s property is a strong differentiator. For investors, it means better liquidity, faster sales turnaround, and higher negotiation leverage during resale.

Sustainability and Long-Term Returns

Another dimension to this flexibility is sustainability, now a core component of property valuation. Villas can easily incorporate eco-efficient technologies that reduce utility costs and attract environmentally conscious tenants.

For example:

- Smart thermostats and solar systems can lower utility bills by up to 25%.

- Dewa-registered solar panels can reduce electricity costs and add compliance value under Dubai’s Shams Initiative.

These improvements not only improve cash flow but also align with Dubai’s 2040 Urban Master Plan, which emphasizes green living and energy efficiency — further enhancing villa asset desirability over time.

Investor Insight

Reduced maintenance costs and upgrade autonomy are more than conveniences — they are profit multipliers.

Where apartment owners operate within rigid expense frameworks and shared liabilities, villa owners retain full agency over operational expenditure and property evolution.

For a discerning investor, this translates into:

- Higher net yield efficiency (fewer deductions per rental dirham).

- Appreciation leverage through value-added upgrades.

- Faster resale and stronger negotiation power.

In essence, villas and townhouses are living, flexible assets — capable of adapting to owner strategy, market conditions, and design trends. Apartments, in contrast, are static holdings.

And in a market that increasingly rewards innovation and sustainability, control equals profitability.

6. Lifestyle Appeal and Tenant Retention: The Hidden Engine of Real Estate Profitability

In real estate investing, numbers often dominate the conversation — yields, appreciation rates, service charges, and return on equity. Yet one of the most powerful, and often underestimated, forces driving profitability is tenant retention. The duration and stability of a tenancy can determine whether an asset delivers consistent, compounding income or fluctuates with every renewal cycle.

Within Dubai’s residential landscape, villas and townhouses consistently outperform apartments in tenant retention, turning them into silent engines of financial stability.

The Retention Advantage: Longer Leases, Lower Turnover

According to CBRE’s 2025 Q2 Residential Market Review, the average tenancy duration in villa and townhouse communities now ranges from 3.5 to 4 years, compared to just 1.8 years for apartments. This difference may appear small, but its financial impact is substantial.

Every time a tenant vacates, the landlord faces downtime, repainting or maintenance expenses, and brokerage fees — costs that can consume up to two months of annual rent. When turnover occurs annually, these recurring expenses can erode as much as 10–12% of net returns.

Villas, by contrast, attract tenants who view the property not as a temporary residence but as a home. They invest emotionally in the space — personalizing gardens, enrolling their children in nearby schools, and forming long-term social ties within the neighborhood. Consequently, they rarely relocate unless they are purchasing their own property.

This behavioral difference — between temporary occupancy and community integration — is what makes villa leases far more durable, predictable, and valuable from an investor standpoint.

The Psychology of Staying: Why Families Commit

The villa and townhouse lifestyle appeals directly to the priorities of Dubai’s growing family demographic. These residents are typically middle- to upper-income expatriates, often on long-term or Golden Visas, seeking permanence and comfort. They choose homes that align with family-centric aspirations — privacy, space, safety, and access to essential services.

Communities such as Dubai Hills Estate, Arabian Ranches, Mudon, and The Meadows are designed around this ethos:

- Tree-lined streets and landscaped parks for recreation.

- Gated perimeters ensuring security and peace of mind.

- Proximity to reputable schools, clinics, and supermarkets.

- Clubhouses, community centers, and sports facilities that foster belonging.

This integration of lifestyle, infrastructure, and community creates an ecosystem that encourages long-term residency. Once families settle into these environments, relocation becomes disruptive — emotionally, logistically, and financially — leading to high renewal rates and low vacancy.

The Financial Impact of Retention

From a purely economic perspective, steady tenancy equals consistent income. Villas with long-term occupants enjoy minimal rent gaps between leases, fewer brokerage commissions, and lower wear-and-tear expenses due to more responsible occupancy.

For instance, in a villa with a four-year tenancy, an investor avoids three years of agency fees, repainting, and vacancy periods that an apartment landlord would likely incur under multiple annual turnovers. The compounded savings can increase effective net yields by 1.5–2% annually — a significant boost to long-term ROI.

In addition, steady cash flow makes financing more efficient. Banks view consistent rental histories favorably, often allowing villa owners to secure better refinancing terms or equity release options compared to properties with frequent tenant churn.

Community Retention as a Value Driver

Tenant retention also contributes to community value stability. Neighborhoods with consistent long-term residents maintain better upkeep, security, and reputation — factors that reinforce both rental demand and resale liquidity.

This self-reinforcing cycle — where quality residents attract further quality demand — is a hallmark of mature villa developments such as Arabian Ranches, The Lakes, and Jumeirah Park.

In contrast, apartment clusters with transient tenant bases can suffer from inconsistent maintenance and service standards, leading to faster depreciation of both asset value and rental perception.

Emotional ROI: Beyond the Spreadsheet

The economics of tenant retention extend beyond rent receipts. Long-term tenants contribute to the intangible value stability of an asset. They treat the property with care, maintain its condition, and build relationships of trust with landlords.

This emotional ROI — rooted in satisfaction, belonging, and security — converts directly into financial ROI. An emotionally anchored tenant is a financially stable one: they pay on time, renew willingly, and maintain the property responsibly. In a market as dynamic as Dubai, where supply shifts rapidly, such tenants are the ultimate insurance against volatility.

Investor Insight

In the evolving landscape of Dubai real estate, villas and townhouses offer more than superior yields — they deliver durable income through lifestyle-driven loyalty.

Where apartments rely on high turnover to sustain revenue, villas thrive on continuity. Every year a tenant renews, an investor saves costs, compounds profit, and strengthens the long-term viability of their portfolio.

Emotional satisfaction and lifestyle security translate directly into financial stability.

In other words, villas do not merely generate rent — they cultivate relationships that keep returns resilient and predictable across market cycles.

7. International Demand and Global Capital Flows: Dubai’s Safe-Haven Status Redefined

Dubai’s real estate market remains one of the most globally magnetized property sectors in the world — a safe-haven destination that blends economic resilience, lifestyle appeal, and tax efficiency. Over the past several years, it has evolved from a transactional investment hub into a long-term capital preservation market, attracting not just speculative buyers, but end-user families, entrepreneurs, and global high-net-worth individuals seeking permanence and quality of life.

Dubai as a Global Investment Magnet

Across every major property cycle, Dubai has demonstrated a unique capacity to attract cross-border investment even amid global volatility. With its strategic geographic location, political neutrality, and open economic policies, the city has become a preferred real estate hub for capital inflows from Europe, Asia, and the Middle East.

Data from Knight Frank and JLL confirm that international buyers account for approximately 40–60% of villa transactions in several leading master communities — a proportion that continues to rise as more investors seek tangible, secure, and lifestyle-enhancing assets.

Countries such as the UK, Russia/CIS, India, China, and Western Europe remain the strongest sources of inbound capital. However, a new wave of high-income professionals from North America and the Asia-Pacific region has also begun entering the market, particularly in prime villa clusters offering family-scale living and long-term visa pathways.

Villas as the Preferred Entry Point for Global Buyers

For international investors, villas and townhouses represent more than just real estate — they signify permanence, security, and a lifestyle upgrade.

The ability to own freehold property in master-planned, family-friendly environments differentiates Dubai from other global investment destinations, where restrictions on foreign ownership and high taxation often limit investor appeal.

The AED 2 million threshold for property-linked Golden Visa eligibility has made villas the natural entry point for relocation-minded investors. These buyers typically prefer assets that combine space, privacy, and long-term residency benefits, allowing families to live, work, and educate their children in Dubai without frequent visa renewals.

Developments such as Palm Jebel Ali, Sobha Reserve, Emaar South, Tilal Al Ghaf, and Damac Lagoons are prime examples. Each offers large-scale villa inventory integrated with leisure, education, and retail facilities — appealing to foreign families who prioritize both livability and capital stability.

In many of these projects, overseas investors represent up to 60% of total sales, underscoring how Dubai’s villa market has become an internationally recognized wealth preservation vehicle rather than a speculative asset class.

The Evolution from Investment to Residency

While apartments historically attracted investors seeking quick returns and rental income, the global buyer profile in Dubai is evolving.

Today’s international purchasers view villas not as short-term income generators but as multi-generational residences and lifestyle anchors. Many are professionals establishing business bases in the UAE or families relocating from regions facing economic or political instability.

Dubai’s appeal lies in its combination of safety, infrastructure, and lifestyle, all reinforced by:

- A tax-free environment for property ownership and capital gains.

- World-class healthcare, education, and hospitality.

- Proximity to global transport hubs with direct access to 200+ cities.

- A stable currency pegged to the U.S. dollar, insulating wealth from currency risk.

This convergence of factors positions Dubai villas as both a lifestyle upgrade and a strategic global asset allocation, comparable to premium properties in London, Singapore, or Miami — yet often at a fraction of their price per square foot.

Investor Profile: Quality Over Quantity

The current wave of international investors differs markedly from previous cycles.

Between 2006 and 2014, most overseas participation in Dubai’s property market came from opportunistic short-term speculators targeting high-rise apartments. In contrast, the 2023–2025 investor profile emphasizes long-term ownership, asset quality, and family functionality.

These buyers typically acquire villas and townhouses valued between AED 3–10 million, often financed through cash or minimal leverage. Their priority is not flipping but lifestyle permanence — a sign that Dubai’s real estate maturity is attracting “patient capital.”

Furthermore, the rise of digital entrepreneurship, remote work, and global mobility has accelerated migration toward markets like Dubai, where ownership translates into residence, security, and global access.

Resilience Through Global Volatility

Dubai’s ability to attract sustained inflows is particularly significant in the context of global economic uncertainty.

While developed economies face persistent inflation and sluggish growth, Dubai’s GDP growth of 4.8% in 2025 and consistent infrastructure spending reinforce its reputation as a macro-stable environment.

Oil price moderation, diversification into tourism and technology, and regional connectivity continue to draw investors seeking both yield and capital protection. As global capitals tighten real estate regulations, Dubai stands out as a pro-investor jurisdiction, offering clarity, liquidity, and unrestricted foreign ownership in dozens of master communities.

Investor Insight

The shift in global capital flows tells a clear story:

Dubai has moved from being a speculative investment hotspot to a global residency and wealth destination.

Villas and townhouses now serve as the bridge between financial investment and lifestyle migration — assets that protect capital while enhancing quality of life.

Where apartments symbolize short-term opportunity, villas represent long-term security, legacy, and permanence.

For international investors, the equation is simple:

Land, lifestyle, and longevity — the Dubai villa market offers all three.

8. Developer Strategy: The Rise of Horizontal Living

Dubai’s property development strategy is undergoing a structural transformation. The city that once symbolized vertical ambition through its towering skyscrapers and skyline-defining landmarks is now moving decisively toward horizontal master-planned communities. This shift reflects a growing recognition among developers and policymakers that livability, sustainability, and long-term residency appeal are the new currencies of real estate value.

From Towers to Townships

For the past two decades, Dubai’s urban identity was built on vertical density — the engineering marvels of Downtown Dubai, JLT, Business Bay, and Marina captured the world’s imagination. But as the population expands and demographic trends evolve, the appetite for high-rise living has matured.

Today’s end-users and family investors increasingly seek spacious, low-density environments — communities that combine suburban tranquility with city-level connectivity.

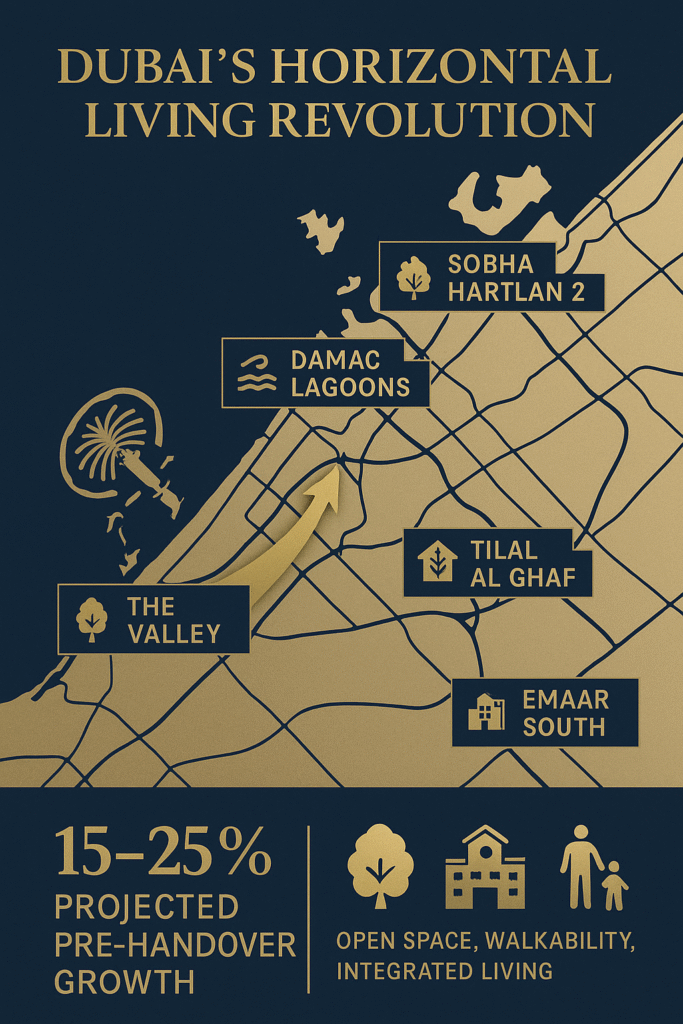

Leading developers such as Emaar, Majid Al Futtaim, Damac, and Sobha Realty are reorienting their strategies to meet this demand. Their latest launches — The Valley, Tilal Al Ghaf, Damac Lagoons, Sobha Hartland 2, and Emaar South — emphasize open spaces, green corridors, walkability, and integrated amenities, redefining what it means to live in modern Dubai.

Design Philosophy: The “Live, Work, Play” Ecosystem

These new horizontal developments are more than just villa clusters — they are self-sustained lifestyle ecosystems designed for multi-generational living.

Common design principles include:

- Integrated green belts and parks to encourage outdoor recreation.

- Pedestrian-friendly pathways linking homes to retail, schools, and mosques.

- Community centers, gyms, and water features that promote social interaction.

- Smart infrastructure such as solar lighting, water recycling, and district cooling.

This design philosophy not only improves livability but also supports long-term property value appreciation by reducing environmental strain and fostering community cohesion. Developers understand that the future buyer is not merely seeking square footage — they are seeking a balanced lifestyle.

Capital Appreciation in Early Phases

One of the most compelling aspects of investing in horizontal developments is the pre-handover appreciation potential.

As infrastructure, landscaping, and community amenities gradually come to life, property values tend to increase in tandem.

Case in point:

- Townhouses in Damac Lagoons that launched at AED 1.4 million in early 2023 are now reselling for AED 1.8–1.9 million, reflecting 20–25% appreciation even before completion.

- The Valley by Emaar saw early-phase buyers gain AED 300,000–500,000 in value within just 12 months of the launch, driven by robust demand and limited supply of comparable low-density units.

This “construction-phase uplift” offers investors a unique opportunity to capture capital gains before handover, often outperforming rental yields during the same period.

Community-Led Growth and Demand Durability

Horizontal communities also create self-sustaining demand loops. Once a community’s initial phases are occupied, local demand grows organically from residents seeking to upsize within the same area — a trend visible in Arabian Ranches, The Springs, and The Lakes.

Developers strategically phase their projects to maintain demand momentum while scaling amenities over time. This results in steady price growth and long-term defensiveness even during market slowdowns. The consistent end-user base in these neighborhoods reduces volatility and ensures strong resale liquidity.

Urban Accessibility Meets Suburban Calm

A major appeal of these new villa clusters is their strategic placement along Dubai’s expanding arterial road network. Communities such as The Valley (along E66), Tilal Al Ghaf and Damac Lagoons (off Hessa St), and Emaar South (near Al Maktoum International Airport) provide direct access to key employment zones while maintaining suburban peace.

With upcoming infrastructure projects like the Dubai Metro Blue Line, expansion of Al Maktoum Airport, and the Expo City smart mobility network, these areas are expected to see enhanced connectivity and sustained demand over the next decade.

Investor Insight

Investing early in horizontal master developments provides a two-tier return advantage:

- Capital growth during construction, as infrastructure and amenities mature.

- Long-term value stability post-handover, supported by lifestyle-driven end-user demand.

In essence, horizontal developments represent the evolution of Dubai’s real estate market — from speculative vertical towers to sustainable, community-centered townships.

For investors, they offer the best of both worlds: growth during build-up and resilience after maturity.

9. Market Cycle Resilience: The Defensive Power of Land-Based Assets

Dubai’s real estate market is famously dynamic — shaped by waves of global capital, developer supply cycles, and macroeconomic shifts. Yet across every expansion and correction since 2010, one trend remains consistent: villas and townhouses outperform apartments in both downturn protection and recovery speed.

This resilience is rooted not in speculation but in fundamental livability demand, end-user ownership, and constrained land supply.

Understanding Dubai’s Market Cycles

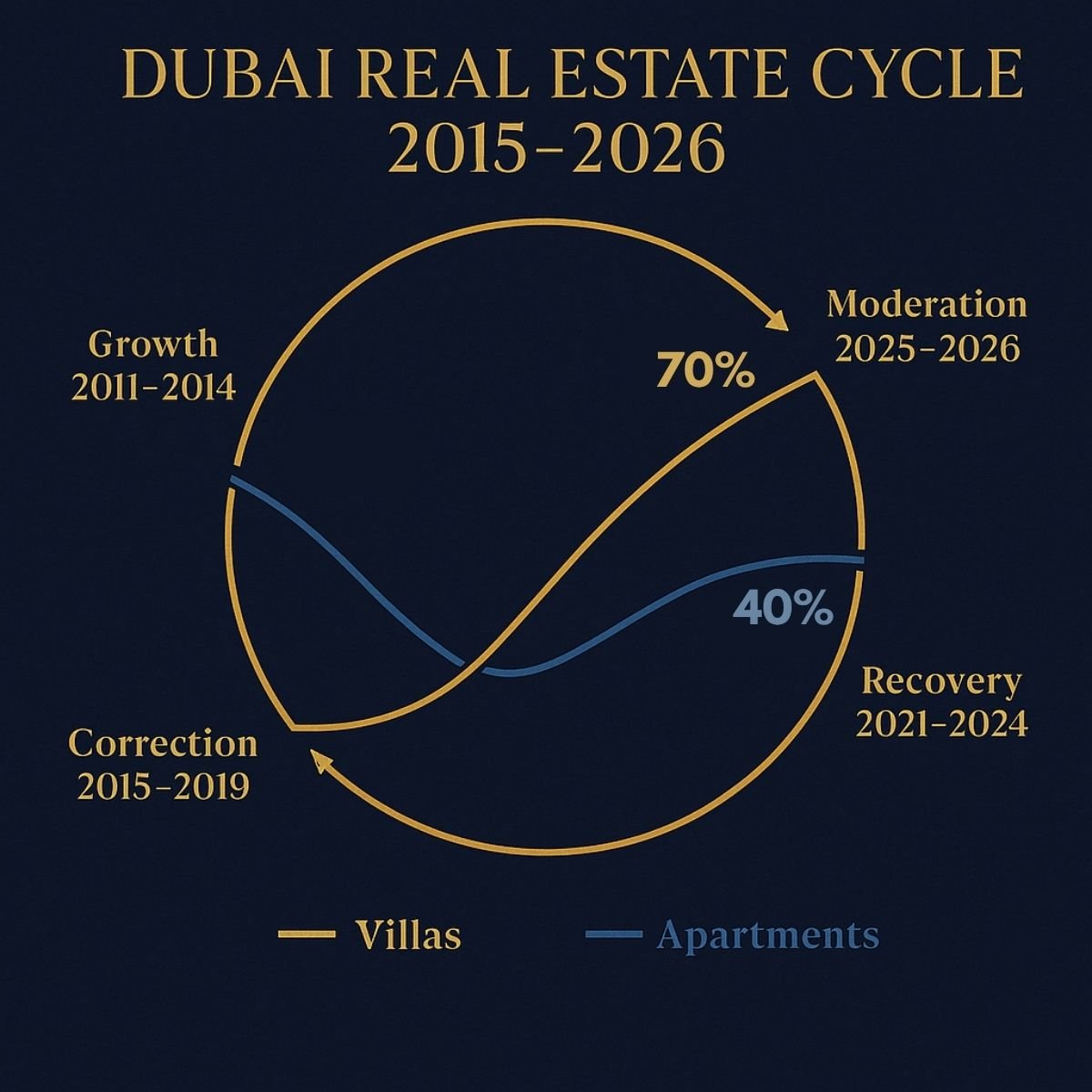

To appreciate the resilience of villas, it’s important to view Dubai’s property market through its historical cycles:

| Market Phase | Period | Apartment Performance | Villa Performance | Key Dynamics |

|---|---|---|---|---|

| Growth Cycle I | 2011–2014 | +55% | +48% | Post-GFC rebound, heavy off-plan launches |

| Correction Phase | 2015–2019 | –25% | –12% | Oversupply, oil price drop, global slowdown |

| Pandemic & Recovery | 2020–2022 | +35% | +65% | End-user migration, space demand, low interest rates |

| Maturity & Expansion | 2023–2024 | +40% | +70% | Record inflows, Golden Visa, supply constraints |

| Moderation Cycle | 2025–2026 (forecast) | Stabilization / –5% to +3% | Stable / +5% | Demand normalization, focus on quality & yield |

Key takeaway: While apartments experience deeper troughs and more volatile peaks, villa values move within narrower bands, preserving equity during corrections and outperforming during rebounds.

Why Villas Lead in Downturns

The reason villas remain more stable is structural:

- Limited Supply: Unlike apartment towers, villa stock cannot be mass-produced. Development requires significant land allocation and longer construction timelines, which naturally cap supply.

- End-User Ownership: Villa buyers are typically residents or families — less likely to liquidate during short-term fluctuations. Apartments, by contrast, are heavily investor-driven and more susceptible to panic selling.

- Lifestyle Stickiness: Villas offer tangible lifestyle value — space, privacy, and comfort — making them essential-use assets rather than speculative ones.

- Maintenance Flexibility: Lower recurring costs enable owners to hold longer through downturns without yield erosion.

The cumulative effect: villas are less price-elastic — meaning their values respond more gradually to market pressures, cushioning investors from sharp losses.

The 2015–2019 Correction: A Case Study

Between 2015 and 2019, Dubai’s real estate market corrected after years of overbuilding and softening oil prices. Apartment prices fell by roughly 25%, exacerbated by new high-rise deliveries and investor exits.

Villas, however, recorded an average decline of just 12%, according to ValuStrat. Communities such as Arabian Ranches, The Meadows, and Jumeirah Park showed remarkable stability, supported by strong rental demand and low resale availability.

This cycle demonstrated the inherent elasticity of end-user–driven assets: families continued to buy and rent villas despite broader market uncertainty, preventing steep devaluation.

The 2021–2024 Recovery: Villas Lead the Rebound

Fast forward to 2021, and the trend reversed powerfully. As global travel resumed post-pandemic and Dubai emerged as a relocation magnet, villas became the centerpiece of the recovery.

Driven by remote working trends, Golden Visa reforms, and lifestyle migration, villa values surged by over 70% between 2021 and 2024 — outpacing apartment appreciation (+40%) by nearly 30 percentage points.

Prime villa districts such as Palm Jumeirah, Dubai Hills, and Tilal Al Ghaf saw record-breaking transactions, with limited inventory and rising international participation. Villas became not only homes but wealth-preserving assets, solidifying their status as Dubai’s “blue-chip” real estate class.

2025–2026: Stability in a Cooling Market

As the market transitions into a moderation phase, analysts from JLL, CBRE, and Knight Frank project a flattening of prices across mid-tier apartment segments due to rising supply.

Villas, however, are expected to retain stability and record modest appreciation of 3–5% annually, supported by constrained supply, end-user absorption, and growing relocation-driven demand.

Communities with strong infrastructure and connectivity — such as The Valley, Damac Lagoons, and Emaar South — are positioned to outperform, as they combine affordability with master-planned amenities.

Investor Perspective: Defensive Allocation

In investment strategy terms, villas act as the defensive asset class within Dubai’s property portfolio — similar to how blue-chip equities or gold behave in financial markets.

While apartments deliver higher liquidity and initial yield, villas provide capital safety, slower depreciation, and long-term appreciation.

This distinction is crucial for institutional and individual investors looking to balance portfolios between growth and protection:

- Apartments: Short-term yield, higher volatility.

- Villas: Long-term equity growth, lower volatility.

In a diversified real estate strategy, allocating a portion to villas provides natural risk hedging against market swings and speculative oversupply.

Investor Insight

Villas are built on scarcity and necessity, not speculation.

Their performance across multiple market cycles confirms that they function as the most reliable hedge against volatility in Dubai real estate.

For investors entering the 2025–2026 phase, where the broader market may cool from record highs, villas and townhouses remain the anchor of portfolio stability and wealth preservation.

“When markets fluctuate, land holds value; when sentiment fades, lifestyle sustains demand.”

Conclusion: The Future Belongs to Horizontal Living

Dubai’s real estate landscape has matured from its early years of speculative vertical expansion into a globally admired model of livability, end-user depth, and sustainable value creation. The city’s evolution from a skyline of high-rises to a network of master-planned villa communities signals a fundamental redefinition of what constitutes real estate success in the UAE.

Across every market cycle — from the corrections of 2015–2019 to the unprecedented recovery between 2021 and 2024 — one theme has remained consistent: land-based, low-density assets outperform high-rise investments in both resilience and long-term appreciation. Villas and townhouses are no longer niche lifestyle products; they are the core of Dubai’s future residential strategy.

Driven by structural demand from families, global relocations, and policy incentives like the Golden Visa, Dubai’s villa market embodies permanence. It represents not only a financial asset but also a lifestyle promise — a commitment to space, security, and community in a rapidly urbanizing world.

From a purely investment standpoint, the numbers tell a compelling story:

- Capital Growth: Villas have appreciated ~72% since 2021, outperforming apartments by nearly 30 percentage points.

- Yield Efficiency: Townhouses and villas now deliver 5.8–7.0% net yields, surpassing apartments when adjusted for service charges.

- Market Stability: Villas experience milder downturns and lead recoveries, consistently acting as the market’s defensive backbone.

- End-User Depth: Families and long-term residents now account for nearly half of villa transactions, ensuring sustained occupancy and demand stability.

These dynamics illustrate a market no longer dependent on speculation, but anchored in end-user fundamentals and quality-of-life economics. Dubai’s leading developers — Emaar, Damac, Sobha, and Majid Al Futtaim — have already aligned their pipelines accordingly, shifting billions in investment toward horizontal, integrated communities that will define the city’s next decade of growth.

For investors, the opportunity is both strategic and time-sensitive. Entering early into villa and townhouse developments — especially within emerging zones like The Valley, Damac Lagoons, Emaar South, and Tilal Al Ghaf — provides dual benefits:

- Short-term capital appreciation during construction and infrastructure rollouts.

- Long-term defensiveness once communities mature and end-user absorption consolidates.

The trajectory is clear. As global wealth migrates toward markets offering transparency, safety, and residency access, Dubai’s horizontal residential sector stands as a safe, appreciating, and lifestyle-driven asset class.

Where high-rises symbolize transience, villas symbolize tenure. Where speculation fades, community endures. And where volatility challenges short-term investments, land and lifestyle secure lasting value.

In the new era of Dubai real estate, growth is not measured by height — but by depth, quality, and the permanence of value.