What exactly is SOL Luxe?

SOL Luxe is a high-rise (G+~62) mixed-use tower on Sheikh Zayed Road (Trade Centre First) with 1–3BR apartments above commercial floors. Marketing and broker sheets consistently show starting prices from ~AED 1.9M and a Q4-2028 handover; common plans publicized include 5/45/50 (or 50/50 type variants). Binayah Properties

Sol’s own site positions it as a new icon on SZR (prime corridor, metro/DIFC/Dubai Mall reach). Sol Properties

Why investors look at it

- Tenant depth: Immediate catchment of DIFC / Dubai Mall / Metro (executive/consulting/finance/legal tenants).

- Ticket vs address: SZR story at a mid-prime ticket (vs ultra-prime icons).

- Staged equity: 2028 delivery can improve IRR if you deploy capital in tranches and avoid paying for dead time on a completed ultra-prime asset.

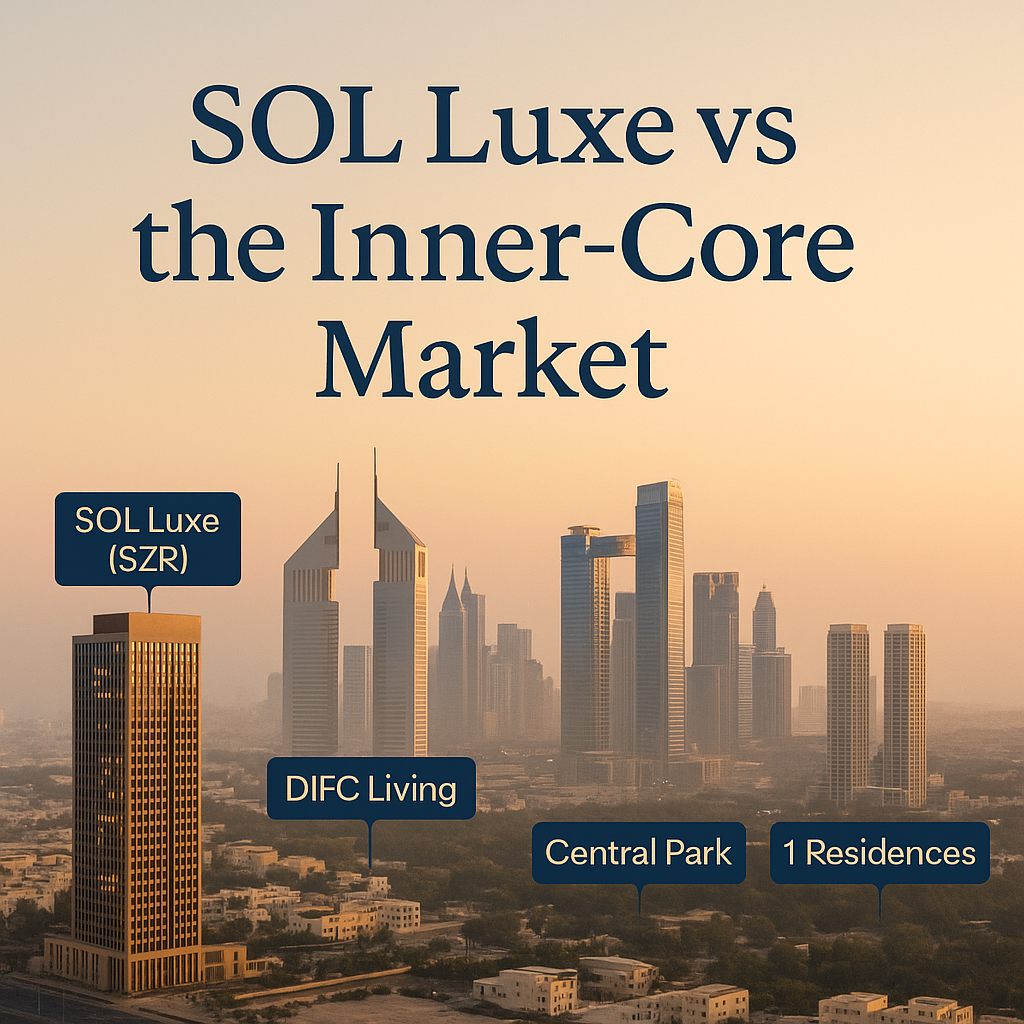

The comparison set (and why these 4)

| Project | Where & what | Handover / Status | Typical payment / price signal | Relevance |

|---|---|---|---|---|

| SOL Luxe (SZR / Trade Centre First) | SZR address; 1–3BR exec-rental tower | Q4-2028 (off-plan) | From ~AED 1.9M, 5/45/50 seen in market | Baseline |

| DIFC Living | Inside DIFC; business-district pedigree | Q3-2026 (off-plan) | 70/30 with 5% booking per multiple sources | Earlier income in the same talent pool |

| One Za’abeel – The Residences | Zabeel 1 icon; completed Dec-2023 | Ready | Listings often AED 5.2M+ entry; trophy | Ready ultra-prime alternative |

| Central Park (City Walk) | Inner-core park-lifestyle by Meraas | Phase handovers ~2027 | Developer-released per phase | Lifestyle play near SZR |

| 1 Residences (wasl1) | Zabeel Park edge, transit-linked | Ready (Q2-2022) | Resale driven | “Income now”, lower construction risk |

Sources: Sol Luxe positioning, Q4-2028 & price; DIFC Living Q3-2026 & 70/30; One Za’abeel completion & pricing; Central Park 2027 phases; 1 Residences completion Q2-2022. Off-Plan Properties Dubai

Micro-location demand & rentability

- SOL Luxe (SZR / Trade Centre First): Fast walk/short hop to DIFC and Metro → deep pool of 1–2BR executive tenants and potential corporate leases. Expect faster stabilization post-handover vs fringe communities because commute time is the #1 amenity in this segment. TopLuxuryProperty.com

- DIFC Living: Inside DIFC itself, so the corporate demand is even more concentrated; trade-off is earlier cash calls (70/30) and generally DIFC-premium pricing. Bayut

- One Za’abeel: UHNW/corporate housing and prestige end-users; yield is naturally tighter given high entry price and trophy status, but leasing starts immediately. Bayut

- Central Park (City Walk): Inner-core greenery + lifestyle; family-friendly 2BR demand and strong end-user absorption; income likely before Sol Luxe (2027 vs 2028). Meraasw

- 1 Residences (wasl1): Parks-edge commuter base; ready since Q2-2022 so zero construction risk and income now. Opr

Payment-plan math & IRR (what the timing really does)

Sol Luxe (2028)

- Marketed plans show 5/45/50 or 50/50 types: low booking, staged progress payments, large handover balloon. Less equity tied up early → potentially higher IRR if the market is constructive at delivery. TopLuxuryProperty

DIFC Living (2026)

- 70/30 with 5% booking, Q3-2026 completion. Income ~2 years sooner, but much more front-loaded equity (and sooner SC/fit-out costs). Bayut

One Za’abeel (ready)

- Income now; no delivery risk; you pay the time value via high ticket (listings commonly AED 5.2M+). IRR relies on rental plus capital preservation. Property Finder

Central Park (2027)

- Splits the difference on timing; lifestyle edge attracts end-users and renters; check each phase’s exact handover. DrivenProperties

1 Residences (ready)

- Immediate leasing; pricing driven by secondary market; check service charges and actual transacted comps. Opr

Cost stack that moves net yields (use this checklist)

- Service charges (SC): Prime corridor towers usually carry higher SC than community assets. For underwriting, model ±3 AED/sqft on any stated guidance; this single input can swing net yields by 100–150 bps on 1–2BR units. (Get written SC guidance from the latest release.)

- Vacancy & lease-up: Assume 1–2 months in Year-1 for off-plan handovers; executive corridors usually stabilize faster (pre-market 60–90 days ahead).

- Leasing costs: Agency, marketing, staging, snagging/rectification.

- Finance & opportunity cost: If you keep dry powder during construction, measure IRR vs a ready purchase’s earlier income.

- Exit friction: Pre-handover assignment rules/fees (if you plan to flip) vary by SPA; check before booking.

Scenario modeling (illustrative logic, not price advice)

Target unit: 1BR executive-rental stack

- Sol Luxe 1BR (mid-prime SZR address, 2028 handover) → Expect gross yield > DIFC ultra-prime on lower ticket, but SC and 2028 cluster risk matter.

- DIFC Living 1BR (inside DIFC, 2026) → Sooner rent, stronger corporate depth, but IRR can compress if the 70/30 schedule front-loads equity without a big discount.

- One Za’abeel 1–2BR (ready, trophy) → Tightest cap rate; thesis is prestige + liquidity + income now.

- Central Park 1–2BR (2027) → Lifestyle premium; good end-user and rental blend; earlier income than 2028.

- 1 Residences 1–2BR (ready) → “Yield now” with parkside story; check current achieved rents and SC.

Where SOL Luxe wins

- Address that rents: SZR/DIFC/Metro adjacency = deep executive pool and corporate leasing prospects, helping fast stabilization. TopLuxuryProperty.com

- Ticket vs iconics: You sell a recognisable core-city story at ~AED 1.9M+ (often far below ultra-prime ready icons like One Za’abeel with AED 5.2M+ entry). Binayah Properties

- Staged equity to 2028: If you’re optimizing cash flow through construction, the plan cadence can raise IRR vs paying for a ready unit today (but you take delivery/supply risk). TopLuxuryProperty.com

Where it doesn’t (trade-offs)

- Later income: 2028 vs DIFC Living 2026 or Central Park 2027 means you wait longer for rent; weigh against staged equity benefits. Bayut

- SC sensitivity: Prime corridor towers’ operating costs can narrow net yields; always underwrite on net.

- Assignment & exit: If a pre-handover flip is part of your thesis, confirm SPA assignment policy/fees up front.

Stack selection playbook for SOL Luxe (picking the right line)

- 1–2BR sweet spot for DIFC-adjacent tenants (optimize rentability vs SC).

- Prioritize view lines with living-room exposure (Burj / sea where available) to support rent and exit pricing.

- Avoid low floors near mechanicals/loading and check lift-to-unit ratios (noise, wait times).

- Parking & access: predictable SZR ingress/egress; 5–7 min walk to Metro matters for executive leasing propositions. TopLuxuryProperty.com

Risk register (inner-core cluster) & mitigations

| Risk | How it shows up | Mitigation |

|---|---|---|

| Handover clustering (2027–2028) | Multiple inner-core towers complete; initial leasing incentives rise. | Pre-market units 60–90 days early; partner with relocation/HR desks; stage & professional photos to shorten days-to-let. |

| SC upshift | Higher SC trims net yield. | Get written SC guidance; model ±3 AED/sqft; pick efficient layouts. |

| Macro/IR shocks | Could hit resale/financing around 2028. | Stagger timing (add a 2026/2027 asset); maintain liquidity buffer; plan for 12–18 months hold post-handover. |

| Assignment limits | SPA restricts or prices pre-handover flips. | Confirm assignment terms & fees before booking; plan to hold and rent if needed. |

Verdict (expanded)

If your thesis is executive-rental depth + SZR brand address with staged equity and a 2028 income start, SOL Luxe belongs on your shortlist. You’re paying far less than an ultra-prime ready icon yet selling an address tenants recognize. Just be disciplined on SC, stack selection, and exit optionality. If your KPI is income sooner, DIFC Living (Q3-2026, 70/30) or Central Park (2027) fit better; if you want ready, trophy, immediate income, One Za’abeel is the benchmark—at a much higher entry. Bayut

Source notes (key facts)

- SOL Luxe: SZR/Trade Centre First location, 1–3BR, from ~AED 1.9M, Q4-2028, 5/45/50 or 50/50-type plans (broker/market pages). Binayah Properties

- DIFC Living: Q3-2026 completion; 70/30 with 5% booking reported. Bayut

- One Za’abeel – The Residences: Completed Dec-2023; listings show AED 5.2M+ entries and active transactions. Bayut

- Central Park (City Walk): Meraas developer page; 2027 handovers cited across phase pages. Meraas

- 1 Residences (wasl1): Q2-2022 ready; details from project pages. Opr