Dubai’s real estate market stands at a pivotal juncture as it moves from an era of record-breaking growth into one of structural maturity and recalibration. Over the past three years, property values, rental yields, and transaction volumes have surged to levels unseen since the pre-2014 peak—driven by population inflows, visa reforms, global capital migration, and the city’s enduring appeal as a tax-free investment hub. Yet, as 2025 unfolds, a new narrative is taking shape: one defined not by speculative exuberance, but by data-driven balance, supply discipline, and sustainable growth.

This report analyzes the leading indicators shaping the market’s next cycle—from handover pipelines and mortgage costs to rental dynamics, off-plan absorption, and macroeconomic headwinds. Drawing on recent findings from JLL, CBRE, ValuStrat, Fitch Ratings, and the IMF, it aims to decode where the opportunities and risks truly lie. The purpose is not to forecast a crash or boom, but to map the realistic trajectory of Dubai’s property sector as it transitions into a more measured, globally competitive phase. Investors, landlords, and end-users alike must now navigate an environment where fundamentals, affordability, and strategic timing matter more than ever.

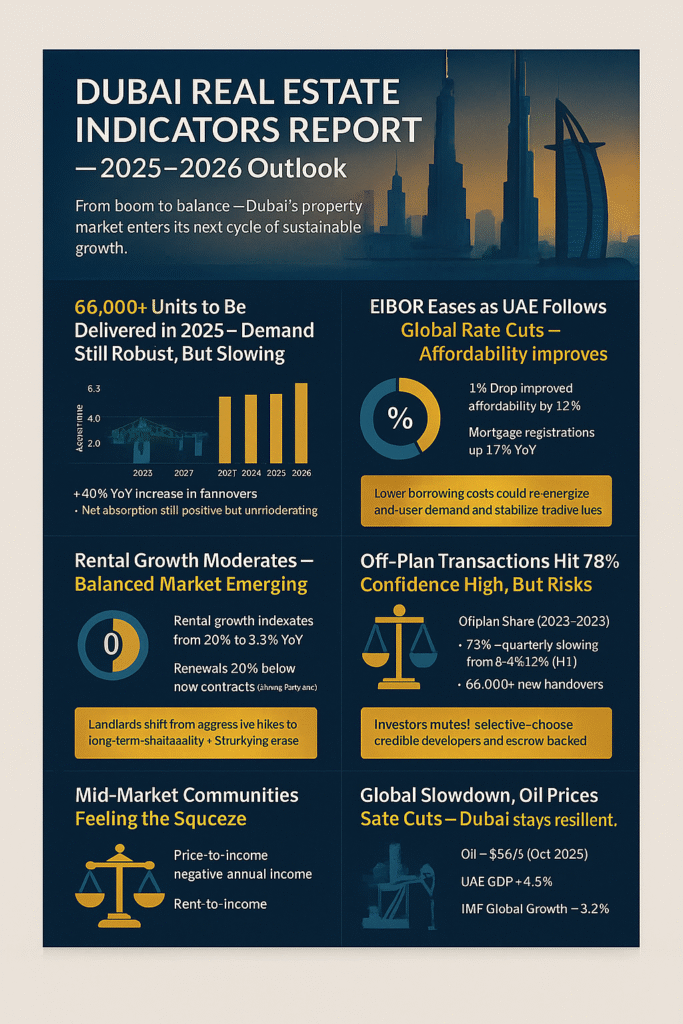

Handover / Supply vs Net Absorption (JLL Framework)

Over the past three years, Dubai’s property market has witnessed one of its strongest construction and delivery cycles since 2014. According to JLL’s UAE Living Market Dynamics Q2-2025, the emirate has entered a phase of normalisation, where new-build handovers are catching up to record demand from 2021–2023. During those pandemic-to-recovery years, absorption exceeded supply, driving rapid price escalation across most freehold zones. Now, as the delivery pipeline swells, the balance is subtly tilting.

Current Dynamics

JLL estimates that by the end of 2025, roughly 66,000–70,000 residential units will be handed over—about 40 percent higher than 2023 levels. Key clusters include Business Bay, Dubai Creek Harbour, MBR City, and Damac Hills 2. In the villa segment, completions remain comparatively modest, preserving scarcity, but the apartment sector faces a multi-year delivery bulge. JLL also highlights that off-plan launches remain elevated, meaning that 2026–2027 deliveries are already being “pre-sold” into today’s market.

Absorption Trends

Net absorption—the measure of new occupied stock—is still positive, supported by population inflows, long-term visas, and job creation in finance, technology, and tourism. However, absorption growth has decelerated from the double-digit surge of 2022. Whereas 2022–2023 saw almost every completed unit absorbed within three months, 2025 data show a rising proportion of unsold ready stock, particularly in peripheral zones like Dubailand and JVC. JLL interprets this as the market’s transition from undersupply to balance, not yet oversupply.

Price & Rent Implications

When completions accelerate faster than absorption, pricing power shifts to buyers and tenants. Developers may increase incentives—longer post-handover plans or fee waivers—to maintain velocity. Secondary owners, seeing more competition, typically face longer days-on-market (DOM) and smaller rent hikes. Thus, while prime areas like Downtown or Palm Jumeirah still enjoy strong absorption thanks to limited new land, mid-market corridors could see a 5–10 percent softening over 12–18 months.

Forward View

JLL’s base case suggests a “soft landing”: continued deliveries, tempered but positive demand, and modest downward pressure on yields. If population growth persists near 3 percent annually, the city can digest most upcoming stock without a crash. However, if global growth falters or off-plan cancellations rise, localized oversupply pockets could emerge. Hence, monitoring the handover-to-absorption ratio remains the single best early-warning indicator of a shift from boom to correction.

Mortgage Rate Trends & EIBOR — Impact on Affordability

Mortgage cost is the financial throttle of Dubai’s ownership cycle. Because the dirham is pegged to the U.S. dollar, UAE rates follow Federal Reserve policy via EIBOR (Emirates Interbank Offered Rate). From 2022 to mid-2024, the Fed’s tightening cycle lifted 3-month EIBOR from ~1 percent to over 5.3 percent, adding roughly 30–35 percent to monthly mortgage payments. This was the hidden brake that cooled secondary-market momentum even as off-plan launches stayed euphoric.

Recent Shifts

By September 2025, the Fed delivered its first 25 bps cut and the UAE Central Bank followed suit. EIBOR eased slightly to around 4.8 percent, signaling the top of the cycle. Banks, flush with liquidity, re-entered competitive pricing—offering fixed-for-two-year loans near 5 percent compared with 6–6.5 percent in early 2024. While that relief is modest, it matters: a one-percentage-point drop improves affordability by ~10–12 percent for a 25-year term loan.

Affordability & Demand Elasticity

End-users, not cash investors, dominate new mortgage registrations. Data from the Dubai Land Department (DLD) show mortgage-backed transactions rising 11 percent YoY in H1 2025, as buyers locked rates anticipating a gradual easing cycle. Each 0.5 percent change in EIBOR translates into about AED 300–400 monthly difference on a AED 1 million loan—material for middle-income families. Thus, affordability defines whether new deliveries are absorbed smoothly or linger unsold.

Broader Economic Linkages

Because Dubai lacks personal income tax, housing costs are the main household expenditure. When EIBOR stays elevated, disposable income contracts, limiting retail and service-sector momentum. Conversely, an easing environment can reignite end-user transactions, supporting steady take-up even amid higher supply. Analysts at Fitch project that if EIBOR averages below 5 percent in 2026, mortgage uptake will rise enough to offset mild price declines.

Credit Quality & System Stability

Unlike 2008, banks now operate under tighter loan-to-value caps (80 percent for expats, 85 percent for Emiratis) and rigorous income-to-debt ratios. Thus, even if affordability tightens temporarily, systemic default risk remains low. This structural resilience limits the probability of a credit-driven crash. Instead, high rates mainly cause demand deferral—buyers wait rather than default.

Outlook

If the Fed delivers two more 25 bps cuts by mid-2026, EIBOR could slide toward 4 percent, reviving sentiment and supporting a gentle re-acceleration in the resale market. If, however, inflation surprises on the upside and rate cuts stall, stretched affordability could force price trimming in the 5–10 percent range across mortgage-dependent segments. Either way, the rate channel ensures that Dubai’s 2025-2026 trajectory will be more cyclical than systemic.

Rent Growth, Vacancy & Days-on-Market (DOM) — CBRE Insights

Rents act as both an affordability gauge and a sentiment barometer. After two years of explosive rental appreciation post-COVID (2021–2023), CBRE’s Dubai Residential Market Review Q2-2025 identified early signs of moderation. Average annual rental growth slowed to 8.5 percent YoY in May 2025, down from >20 percent in mid-2023. Yet vacancy rates remain historically low, meaning the market is cooling, not collapsing.

Renewals vs. New Leases

Dubai’s Rent Index caps renewal increases based on historical rent levels, producing a growing divergence between new lease and renewal rents. CBRE and DLD data show new contracts averaging 20–25 percent higher than renewals, incentivising tenants to stay put. This dynamic suppresses churn: average tenancy duration rose from 1.9 to 2.4 years by mid-2025. As a result, frictional vacancy—the gap between tenancies—remains low at 4–6 percent, well below the ~12 percent long-run norm.

Days-on-Market & Leasing Velocity

CBRE notes DOM rising modestly from 19 days (2023 average) to 27 days by mid-2025 for mid-tier apartments. That is still healthy but signals increasing tenant choice. Prime villas continue to lease within weeks, whereas secondary apartments in outer corridors now sit 6–8 weeks before securing tenants. DOM acts as a lead indicator of rent fatigue: when DOM exceeds 45 days in a community, rental growth typically plateaus within a quarter.

Drivers of Moderation

- New Supply: As JLL observed, new apartment completions add options.

- Affordability Ceiling: Tenants allocate 35–45 percent of income to rent; beyond that, they downsize or shift location.

- Regulatory Stability: The RERA Index framework, while protecting tenants, limits landlords’ ability to fully reprice stock, naturally capping inflation.

- Macro Factors: A stable currency and contained inflation keep real rents from overshooting.

Landlord & Investor Behaviour

With yields compressing slightly—from 6.9 percent average gross in 2023 to 6.2 percent in mid-2025—investors are focusing on retention. Professional management, maintenance speed, and renewal flexibility are emerging differentiators. For tenants, the trend offers relief: double-digit hikes are no longer the norm except in scarce villa sub-markets (e.g., Palm, Jumeirah Islands).

Forecast

CBRE expects overall rents to stabilise through 2025–2026, rising 2–5 percent annually, effectively flat in real terms. Vacancy may edge up to 8 percent as deliveries catch up, but this remains within equilibrium. The market’s cooling trajectory is precisely what sustains long-term health, averting overheating and speculative churn.

Off-Plan Share & Cyclicality (ValuStrat Analysis)

Off-plan sales are the heartbeat of Dubai’s developer economy. ValuStrat’s Dubai Real Estate Review Q2-2025 reported that off-plan accounted for an unprecedented 78 percent of all residential transactions by value—an all-time high. In parallel, the firm recorded record quarterly volumes of both launches and resales of off-plan contracts. While headline numbers illustrate confidence, they also raise concerns about cyclicality.

Understanding the Mechanism

High off-plan share amplifies market sensitivity because it relies on future expectations rather than present occupancy. When sentiment is positive—low interest rates, strong capital inflows—off-plan fuels expansion. When sentiment flips, liquidity in the assignment market evaporates quickly, stranding speculative buyers until completion. Thus, a 70 percent+ off-plan share signals exuberance.

Current Market Characteristics

Developers like Emaar, Sobha, and Damac continue launching at record pace, leveraging generous post-handover payment plans (up to 5 years) and flexible down payments. Buyers, including many foreign investors, treat these plans as leveraged exposure to Dubai’s future growth. However, ValuStrat points out that the quarterly price-growth rate slowed from 4.4 percent (Q1-2025) to 1.7 percent (Q2-2025), implying diminishing marginal returns.

System Buffers

Regulation now requires escrow segregation of buyer funds, limiting systemic risk. Developers cannot divert pre-sale proceeds elsewhere, reducing the “ghost project” problem of 2009. Banks also maintain conservative lending—mortgage finance still represents <25 percent of off-plan volume, meaning most buyers are equity-funded. Hence, while a sentiment correction would hurt resale liquidity, widespread default remains unlikely.

Potential Risks Ahead

- Delivery Wave: ~66,000 units in 2025 and 70,000+ projected 2026 could stress take-up.

- Flip Pressure: Investors who booked at 2023-24 peaks may rush to exit before completion, creating short-term price pressure.

- Secondary Market Crowding: Once delivered, these units swell the ready-stock inventory, affecting resale pricing in comparable communities.

Opportunities

For disciplined investors, this phase enables selective entry into under-construction projects with credible sponsors, where payment schedules align with expected rate cuts. Projects tied to infrastructure catalysts (metro extensions, beach re-masterplans) still hold asymmetric upside.

Forecast

ValuStrat expects off-plan dominance to ease toward 65 percent by late 2026 as completions peak. If EIBOR declines and population inflows persist, the sector can transition smoothly. If not, expect a mid-cycle correction of 10–15 percent in speculative assignments—a healthy re-pricing rather than collapse.

External Shocks — Global Growth, Oil, Geopolitics, Capital Controls

Dubai’s open, trade-centric model makes it one of the world’s most externally sensitive real-estate markets. Four channels dominate: global growth, oil prices, geopolitics, and cross-border capital flow regulation.

Global Growth & Interest-Rate Path

The IMF’s World Economic Outlook Oct-2025 projects global GDP growth of 3.2 percent (2025) and 3.0 percent (2026), a slight uptick from 2024. That benign scenario supports business formation, tourism, and migration—the lifeblood of Dubai’s housing demand. However, any U.S. slowdown or renewed inflation shock could alter the Fed’s rate trajectory, reverberating through EIBOR and mortgages. Thus, macro stability abroad directly affects micro pricing at home.

Oil & Regional Liquidity

Brent crude’s slide to ~$61–62 per barrel (Oct 2025) contrasts with >$80 levels seen a year earlier. Although Dubai’s own economy is non-oil, regional liquidity and investor sentiment correlate strongly with hydrocarbon revenues. Lower oil reduces GCC fiscal surpluses, limiting cross-border property investment inflows. Yet the UAE’s diversification—logistics, finance, tourism—buffers the shock. If oil stabilises above $65 in 2026, liquidity will remain ample; prolonged sub-$60 pricing would test appetite for high-end launches.

Geopolitics & Capital Controls

Ongoing global tensions (Ukraine, Red Sea shipping disruptions) could reshape capital routes. Dubai historically benefits as a safe-haven hub during volatility: inflows from CIS, South Asia, and parts of Europe surged after 2022. However, new anti-money-laundering (AML) frameworks and stricter know-your-client procedures may moderate speculative inflows. That’s ultimately healthy, ensuring durable rather than hot-money demand.

Currency & Comparative Returns

The USD peg means investors from weaker-currency regions (e.g., Eurozone, Pakistan, UK) face higher entry costs when the dollar strengthens. A potential Fed easing cycle may weaken the dollar, improving affordability for these cohorts and partially offsetting local rate effects.

Scenario Outlook

- Base Case: Moderate global growth + oil >$65 → steady capital inflows; Dubai grows 4–5 percent GDP; housing softens modestly.

- Bear Case: Recession + oil <$55 → foreign capital pause; 10–15 percent price dip in mid-tier.

- Bull Case: Fed cuts + global rebound → renewed capital wave; 5–8 percent upside limited to prime zones.

Structural Resilience

Crucially, Dubai now benefits from policy agility: flexible visas, corporate tax reforms, and ESG-linked financing make it less cyclical than in prior eras. The government’s ability to attract skilled migrants underpins constant housing absorption even amid external turbulence. Thus, while global shocks will always ripple through valuations, the emirate’s institutional maturity and diversified demand base ensure volatility results in rotations, not collapses.

Conclusion

The data-driven outlook for 2025–2026 suggests that Dubai’s property market is not heading for a collapse—but rather entering a phase of intelligent normalization. Supply is increasing, but so is the city’s capacity to absorb it through continuous population growth, foreign investment, and robust infrastructure expansion. Mortgage rates are gradually easing, signaling relief for end-users. Rent escalation has cooled, yet remains stable enough to sustain investor yields. And while global economic uncertainty persists, Dubai’s diversification, financial regulation, and visa reforms continue to attract capital from every continent.

In essence, the next cycle will test the discipline, adaptability, and selectivity of market participants. Developers must calibrate launches to genuine demand; investors must prioritize yield and liquidity over speculation; and policymakers must preserve transparency and affordability to protect long-term stability. If these elements align, Dubai’s real estate sector will not merely withstand global volatility—it will emerge as a model of resilient urban growth. The city’s skyline, ever evolving, stands as both a symbol and a forecast: progress continues, but now with a stronger foundation beneath its glittering towers.

Resources & References

1. JLL (Jones Lang LaSalle)

2. CBRE Middle East

- Dubai Residential Market Review Q2 2025 — rental growth, vacancy, and leasing data across key communities.

- UAE Real Estate Market Update 2025 — insights on days-on-market and tenant retention.

3. ValuStrat

4. Fitch Ratings

6. Deloitte Middle East

- Real Estate Predictions 2025: Middle East Edition — structural market reforms, developer strategies, and institutional resilience. https://www.deloitte.com/middle-east

7. Knight Frank

- Prime Global Forecast 2025 — Dubai luxury and branded residence performance outlook.

- UAE Market Pulse 2025 — segmentation between prime and mid-tier markets.

https://www.knightfrank.com

8. Global Property Guide

- Dubai Housing Market Trends 2025 — rental growth data and investment yield analysis.

https://www.globalpropertyguide.com

9. UAE Central Bank (CBUAE)

- Monthly Statistical Bulletin (September 2025) — EIBOR rates, mortgage lending, and macroeconomic indicators.

https://www.centralbank.ae

10. UAE Government & DLD (Dubai Land Department)

- Open Data Portal (Ejari & Transaction Reports) — property transfer data, mortgage volumes, and tenancy trends (2024–2025).

https://dubailand.gov.ae