Executive summary

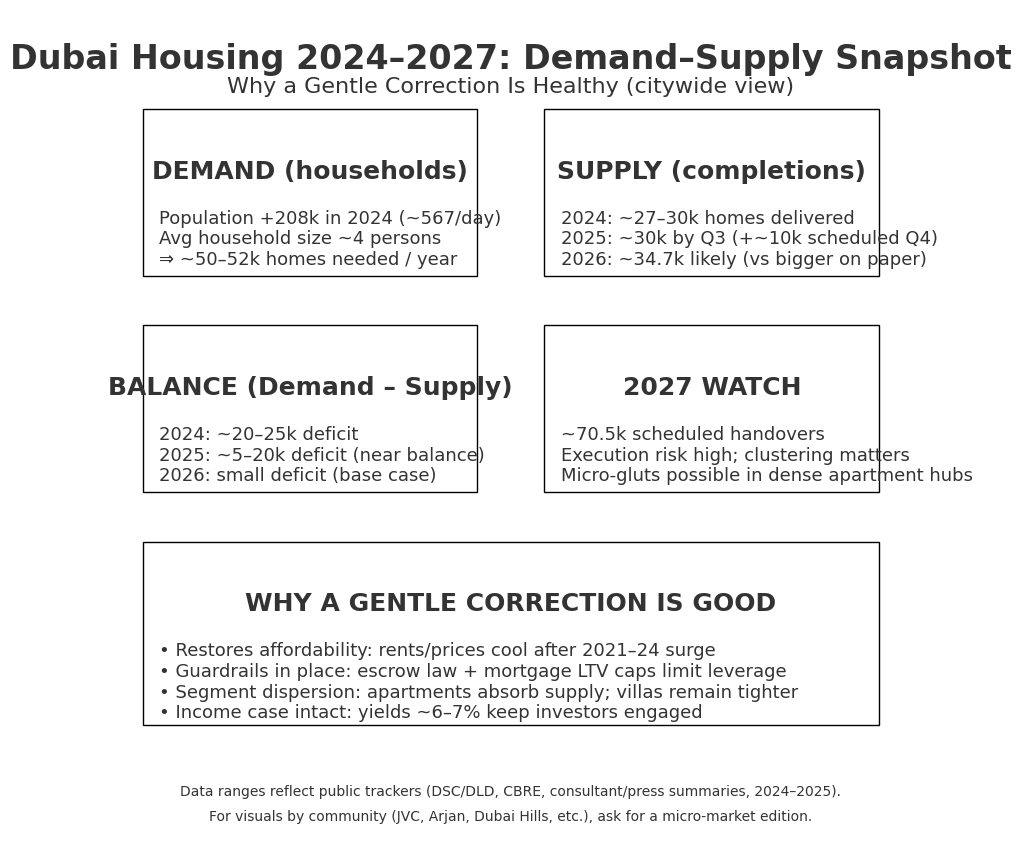

Dubai’s housing demand is anchored by record population inflows and new household formation; supply is catching up but still delivered more slowly than “announced”. In 2024 the emirate added roughly 59,610 new households and over 208,000 residents, equivalent to about 567 extra people per day in early 2025. Using an average household size of ~4 people/home, that implies roughly 50–52k dwellings needed per year just to house newcomers. Actual completions lagged: ~27–30k homes were handed over in 2024, and ~30k had already completed by Q3-2025 with another ~10k scheduled in Q4. Forecasts for 2026 look big on paper, but history suggests only ~48–60% of scheduled units get delivered on time. A measured price correction or period of flat-to-gently-lower prices therefore looks cyclically normal and system-healthy, not a crash. Emirates24|7 Khaleej Times

The demand engine: population, households, and structural inflows

Record household formation

Official data show 59,610 new households created in 2024, taking total households to ~771k, with average household size at 4. This alone implies ~59.6k ÷ 4 ≈ 14.9k homes if every new household were one person—yet Dubai’s average is 4 per household, so each 4-person household equals one home; practically, the same figures corroborate the ~50–52k homes/year demand rule-of-thumb once you translate the 208k net population gain in 2024 into families. Emirates24|7

Macro feeders: jobs, tourism, and the 2040 vision

Policy and macro fundamentals keep pulling people to Dubai: the Dubai 2040 Urban Master Plan targets accommodating ~5.8 million residents by 2040 (from ~3.3m when the plan launched), with a polycentric city layout to match. Meanwhile, the visitor economy keeps the service, retail and hospitality sectors hiring—9.88 million international visitors in H1-2025 alone—supporting rental demand and end-user migration. dubai2040.ae Dubai Department of Economy & Tourism

Bottom line on demand: even if you assume some churn, net household formation is running near 50k homes/year, giving us a stable, quantifiable demand baseline.

The supply side: completions, not launches, pay the rent

2024: solid deliveries, still below demand

Multiple consultancies report different tallies due to scope and methodology; a safe band for 2024 completions is ~27–30k homes (some trackers estimated higher, but Q3-2025 commentary from Savills/press suggests 2024’s delivered volume was roughly ~30k). Either way, it’s below the ~50k homes implied by net household formation—i.e., a material deficit, which explains persistent rental tightness through 2024. Khaleej Times

Note: Some sources earlier estimated ~38k potential 2024 handovers, but realized deliveries appear lower; this is typical in Dubai, where actual handovers trail pipeline announcements. ValuStrat

2025: deliveries accelerate but still chase demand

Savills (via Khaleej Times) indicates ~8,500 units delivered in Q3-2025, taking 2025 YTD completions near 30k, with ~10k more slated for Q4-2025. If achieved, 2025 could end around ~40k deliveries—closer to demand, but still shy of the ~50k “needs” line. Khaleej Times

2026–2027: big numbers on slides; lower on handover day

Morgan’s International Realty (summarised by Khaleej Times) expects only ~34,740 of 71,613 “scheduled” units to actually complete in 2026 (~48% completion rate), after ~22,896 of 37,171 in 2025 (~62%). They see a surge to ~70,537 in 2027 if projects catch up. Track record matters: Fitch also notes that 2022–2024 delivered ~56% of what was initially projected. Khaleej Times

Bottom line on supply: the delivery funnel is widening, but slippage is real. Supply is catching up, not flooding.

The balance: translating people into homes

A simple, transparent framework:

- Demand ≈ net new households

2024: +~208k people → ~50–52k homes needed (assuming ~4 persons/home). Early 2025 maintained a ~567/day run rate, consistent with high demand. Gulf News - Supply = keys handed over

2024: ~27–30k (deficit vs demand).

2025: ~30k by Q3, ~10k scheduled in Q4 (potentially ~40k).

2026: schedule large, but likely ~34,740 realistic.

2027: ~70,537 if construction catches up. Khaleej Times

Conclusion on balance: Deficit in 2024; smaller deficit in 2025; 2026–2027 depend on execution. No persistent glut is visible today at the citywide level, even if some submarkets face temporary micro-gluts.

Prices, rents, and the “healthy correction” narrative

Where prices and rents stand

Mainstream research shows Dubai’s rental growth has begun to moderate in 2025, especially after the rapid run-up of 2022–2024. This is exactly what you expect when deliveries improve and affordability needs attention. CBRE Q3-2025 notes Dubai’s rental growth is moderating even as buyer interest remains healthy. Typical gross yields remain globally competitive (≈ 6–7% overall; higher in apartment districts), which underpins investor holding power. cbre.ae

Why a correction is healthy, not scary

- Affordability valve: After a multi-year surge, flat-to-lower asking prices and cooler rent growth help restore affordability for residents and end-users—critical for sustainable population absorption. CBRE

- Quality of demand improving: More end-user and long-term investors; speculative flipping has already cooled from 2023–2024 peaks, per market commentary. (Press and bank research throughout 2025 discuss lower flipping shares.) Financial Times

- Regulatory buffers: Escrow law (Law No. 8 of 2007) ring-fences off-plan payments, and Central Bank LTV caps limit leverage at purchase—both reduce systemic risk vs earlier cycles. Dubai Land Department

- Segment differentiation: Villa/townhouse stock is still relatively tight versus apartment-heavy pipelines, so any correction skews toward apartment submarkets with clustered completions—again, a localised pressure release, not a citywide bust. Khaleej Times

What independent agencies say

Fitch Ratings expects a moderate correction (up to ~15%) through 2H-2025 to 2026 after peak gains—framed as a normalisation with issuers having rating buffers (i.e., not system-threatening). That is not a crash call; it’s a soft-landing base case. Fitch Ratings

Micro-market watch: where could pressure build?

Morgan’s International Realty highlights JVC, Business Bay, Arjan, Damac Lagoons, and Azizi Venice as areas with heavier scheduled handovers in 2025–2027. Expect pricing/rent competition and longer absorption windows here if a large tranche completes at once. Conversely, low-density villa communities (Dubai Hills Estate, Emirates Living, JGE, prime waterfront) still look supply-constrained, supporting relative resilience. Khaleej Times

Scenario analysis: 2025–2027

Base case (most likely)

- Demand: stays robust on continued in-migration and job creation; tourism strength supports services employment.

- Supply: 2025 ends just shy of balanced; 2026 delivers ~35k ± (if historical completion ratios hold); 2027 spikes if projects catch up.

- Outcome: citywide prices drift sideways to mildly lower in apartment-heavy zones; villas/townhouses largely hold with more modest moves. Gross yields remain 6–7%+. Engel & Völkers+3Khaleej Times+3Khaleej Times+3

Upside case

- Faster-than-expected handovers without demand slowing (e.g., more Golden Visas, corporate relocations), plus REFI and mortgage competition → rent relief and stable values citywide; yields compress slightly as prices firm. CBRE

Downside case (still not a “crash”)

- If financing costs rose sharply or a clustered delivery hits specific districts while demand temporarily softens, apartment prices in those pockets could retrace high single- to low double-digits—in line with Fitch’s moderation call—not a systemic collapse. Regulatory buffers (escrow/LTVs) limit forced selling. Fitch Ratings

Investor takeaways (how to position)

1) Anchor decisions on delivered supply, not glossy launch totals

Completion slippage is structural. Use handovers by community to time entries; expect some Q4-2025 and 2026 projects to push into later quarters. Khaleej Times+1

2) Focus on end-user depth and livability

Assets with schools, healthcare, transit, retail within 10–15 minutes show stickier occupancy and lower vacancy through cycles.

3) Expect yield resilience even as rents cool

With citywide yields ~6–7%, Dubai remains globally competitive; moderate price softness can improve entry yields on new purchases. Engel & Völkers

4) Segment strategy

- Apartments (mid-market, high-density): be selective; price in handover waves in JVC/Arjan/Business Bay, etc. Favor bigger layouts and strong developer service levels to differentiate in leasing. Khaleej Times

- Villas/townhouses: scarcity and lifestyle demand underpin values; target delivery-ready or near-handover projects in proven master plans.

5) Risk controls that didn’t exist in past cycles

- Escrow accounts (Law 8/2007) keep off-plan buyer funds project-ring-fenced.

- Central Bank LTV caps limit leverage (first-home LTVs generally capped; expat vs national rules differ), curbing speculative froth. Dubai Land Department

Frequently asked questions

Is Dubai heading for a market crash?

Unlikely under base-case assumptions. Agencies see moderation (Fitch: up to ~15%) as supply normalises, not systemic stress. Mortgage caps and escrow rules dampen forced selling and developer risk vs earlier cycles. Fitch Ratings

Why do completion numbers differ across sources?

Some count shell & core vs fully handed-over, some include hotel/serviced units, and cut-off dates vary. That’s why we focus on ranges and press-verified tallies like Savills’ Q3-2025 completions. Khaleej Times

Which areas are most at risk of oversupply?

Districts with dense 2025–2027 schedules—JVC, Business Bay, Arjan, parts of DAMAC Lagoons and Azizi Venice—could see temporary pricing pressure at handover. Villas remain relatively tight. Khaleej Times

What keeps demand strong if prices cool?

Population inflows, jobs, tourism scale, plus the Dubai 2040 infrastructure roadmap. Even with a pause, end-user depth and global appeal support absorption. dubai2040.ae

Sources (key references)

- Population & households: Dubai Data & Statistics via Emirates 24/7 (households, avg HH size); Gulf News (208k 2024 increase; ~567/day early 2025). Emirates24|7+1

- Completions & pipelines: Khaleej Times/Savills Q3-2025 (YTD ~30k, ~10k scheduled Q4); Khaleej Times/Morgan’s (2025–2027 handover ratios). Khaleej Times+1

- Macro/visitors: Dubai DET (H1-2025 visitors). Dubai Department of Economy & Tourism

- Policy/vision: Dubai 2040 master plan (official portal + master site). u.ae+1

- Market moderation: CBRE UAE Real Estate Market Review Q3-2025. cbre.ae

- Ratings view: Fitch Ratings (moderate correction; issuer buffers). Fitch Ratings

- Regulation: RERA escrow (Law 8/2007) and CBUAE mortgage LTV framework. Dubai Land Department

Final take

Dubai’s housing story into 2026–2027 is not about collapse; it’s about rebalancing. If you’re allocating capital, think micro-market, insist on sponsor quality, underwrite to conservative yields, and expect two-speed outcomes: firmer where supply is scarce, softer where cranes cluster. That is what a healthy correction looks like—and why it’s exactly what this maturing market needs to power the next leg of growth.