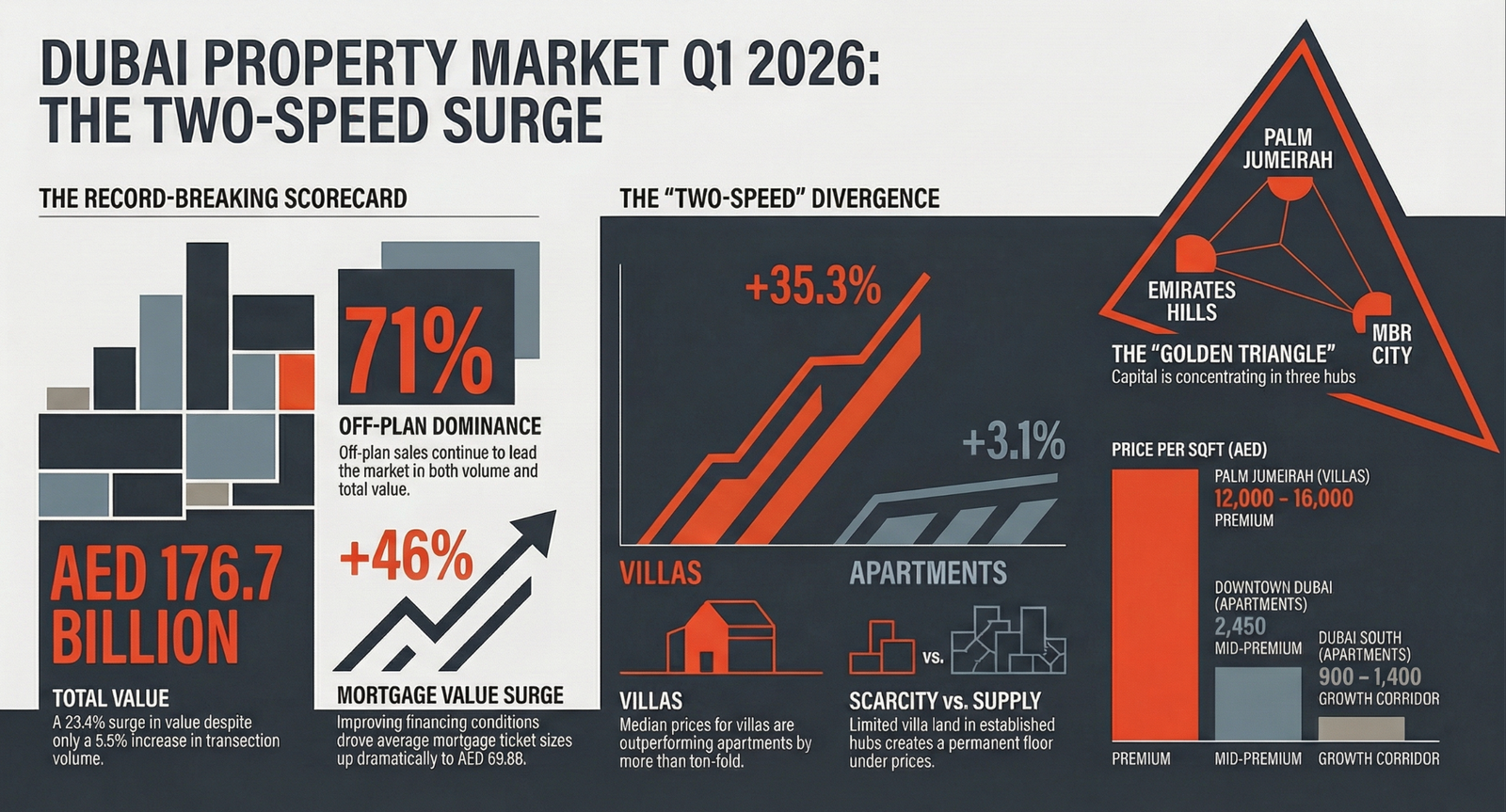

Dubai’s property market posted its strongest first quarter on record in 2026. A total of 47,996 transactions were completed, generating AED 176.7 billion — equivalent to $48.1 billion — in total sales value. Year-on-year, that is a 23.4% jump in value on a 5.5% increase in volume.

The headline numbers are impressive. But they are also misleading if read in isolation. Dubai’s property market in Q1 2026 is not one market. It is two: a villa market running hot and an apartment market warming at a far gentler pace. Overlay the dominance of off-plan launches, a 46% surge in mortgage value, and the emergence of a “golden triangle” that is absorbing a disproportionate share of high-net-worth capital, and the picture becomes considerably more instructive.

This analysis breaks down the Dubai property market Q1 2026 data segment by segment, area by area, so you know exactly which side of this market deserves your attention — and which requires caution.

The Q1 2026 Scorecard

Before unpacking the individual segments, here is the full picture at a glance:

| Metric | Q1 2026 | YoY Change |

|---|---|---|

| Total transactions | 47,996 | +5.5% |

| Total value | AED 176.7 billion | +23.4% |

| Off-plan share (volume) | 70% | — |

| Off-plan share (value) | 71% | — |

| Villa transactions | 8,261 | +17.9% |

| Villa value | AED 59.1 billion | — |

| Mortgage transactions | 11,829 | +7.5% |

| Mortgage value | AED 59.8 billion | +46% |

| Average price per sqft | AED 1,949 | — |

The first thing the scorecard reveals is the value-versus-volume gap. A 23.4% rise in value from only a 5.5% rise in volume means the average transaction value climbed substantially — driven partly by price appreciation and partly by a compositional shift toward higher-value property types, particularly villas.

The Villa Market Is Running Hot

The defining story of the Dubai property market Q1 2026 is villa price appreciation. The median off-plan villa price rose 35.3% year-on-year to AED 4.1 million, while villa transaction volumes climbed 17.9% — making villas both more expensive and more in-demand simultaneously. Total villa value reached AED 59.1 billion across 8,261 deals.

At the luxury end, the appreciation is even sharper. Jumeirah Islands villas rose 41% year-on-year. Palm Jumeirah villas were not far behind at 40%. Emirates Hills and The Meadows logged 27% annual gains. The average Palm Jumeirah villa now changes hands at approximately AED 44.6 million — a 26% rise in twelve months.

Three structural forces are driving this:

Supply scarcity. Developable land for standalone villas within established communities is limited. Unlike apartments, you cannot simply add fifty more floors to Emirates Hills. Once the original plots are sold, new supply is constrained to emerging peripheries — which do not carry the same prestige premium.

End-user preference shift. Post-2020, remote work and lifestyle recalibration drove permanent residents — not just speculators — toward larger living spaces. That end-user demand is stickier than investor demand because it creates real floors under prices: end-users do not panic-sell the way yield-focused investors do when sentiment shifts.

The golden visa effect. Dubai’s five-year and ten-year residency visas — available from AED 2 million and AED 10 million property investments respectively — have created a class of longer-term buyers who treat villas as primary residences. Those buyers tend to cluster in established villa communities and hold for the long term, reducing the tradeable float and amplifying price pressure on available inventory.

The Apartment Market — Steady But Selective

Off-plan apartment prices rose 3.1% year-on-year to a median AED 1.4 million. That is a positive number, but the contrast with the villa market is stark. The key insight is that the apartment market is not underperforming broadly — it is bifurcating internally.

Branded residences and prime-location apartments continue to appreciate meaningfully. Downtown Dubai commands AED 2,450 per square foot, with Burj Khalifa-facing units exceeding AED 3,500 per square foot. Dubai Marina averages AED 2,061 per square foot. These are real capital gains accruing to well-located stock.

Mid-tier off-plan apartments in emerging communities tell a different story. Jumeirah Village Circle has settled at AED 1,050 per square foot. Dubai South ranges from AED 900 to AED 1,400 per square foot. These areas offer accessibility but will face meaningful new supply competition as the estimated 60,000+ units scheduled for 2026 handover filter through.

For buyers, the data suggests a clear sorting rule: location selectivity matters far more in the apartment segment than in the villa segment, where almost all established communities are seeing material gains. Buying the cheapest apartment in a peripheral community to chase a 7% yield is a very different risk profile from buying a villa in Emirates Hills.

The Golden Triangle — Where Serious Capital Is Concentrating

One of the most structurally significant trends emerging from Dubai property market Q1 2026 data is the concentration of high-net-worth buying into three specific areas: Palm Jumeirah, Emirates Hills, and Mohammed Bin Rashid City (MBR City).

Palm Jumeirah alone generated AED 19.38 billion in total sales — 31% of the premium market by value. Emirates Hills contributed AED 9.04 billion, or 15% of that same market. Combined, these two locations accounted for nearly half of all premium transaction value in the emirate during Q1 2026.

MBR City rounds out the trio, with multiple large master-plan villa communities attracting significant institutional and ultra-high-net-worth buyer interest. Together, these three zones form what analysts are calling Dubai’s “golden triangle” — a geographical concentration of wealth that is increasingly self-reinforcing: proximity to other premium buyers sustains prestige values, which attracts more premium buyers.

For investors, the implication is important. Buying within the golden triangle is buying into a structural demand story, not a cyclical one. Entry prices reflect the premium — at an average AED 44.6 million for a Palm Jumeirah villa, yields are compressed relative to the broader market. These are wealth preservation and capital appreciation vehicles, not income-yield plays.

Off-Plan vs Secondary — Understanding the 15% Premium

Off-plan properties carried approximately a 15% premium over comparable secondary-market resale homes in Q1 2026. This may seem counterintuitive — you are paying more for a property that does not yet exist. But the reasons are structural.

Newer builds offer energy-efficient systems, contemporary layouts, and smart-home features that older resale stock cannot easily retrofit. Developer payment plans often require only 10–20% down with the balance spread over construction milestones and beyond handover. And in a rental market where tenants pay premiums for perceived quality, new-build credentials command tangible yield advantages at handover.

Off-plan accounted for 70% of transaction volume and 71% of value in Q1. Secondary market transactions grew a more modest 8% year-on-year, constrained by a persistent bid-ask gap — sellers holding at 2024 peak valuations while buyers anticipate further off-plan launches at competitive prices.

The secondary market’s challenge is simultaneously its opportunity. Patient buyers who can identify motivated sellers in premium communities at prices below current off-plan launches can capture both below-market entry and immediate occupancy or rental income — without the construction risk inherent in off-plan. If you are evaluating any off-plan project, our 18-parameter off-plan de-risk checklist is the place to start.

The Mortgage Surge — What a 46% Jump in Value Signals

One of the most overlooked data points in the Dubai property market Q1 2026 is the mortgage market performance. While transaction volumes rose a measured 7.5% to 11,829 deals, the aggregate value of mortgage lending surged 46% to AED 59.8 billion.

A 46% increase in lending value from a 7.5% increase in transaction count means average mortgage ticket sizes expanded dramatically. There are two drivers. First, higher property prices: as values rise, so does the amount required to finance the same acquisition. This is mathematical. Second, improving financing conditions: as US Federal Reserve rate cuts feed through to UAE lending rates, mortgage affordability improves. Buyers who were priced out at 5.5% borrowing rates are re-entering the market as rates approach sub-5%.

In the resale segment, cash buyers still dominate at 67% of transactions, with mortgage-backed purchases accounting for 33%. But that mortgage share is growing, and as financing conditions continue to ease through 2026, the end-user buyer pool will expand. That broadens demand for secondary-market properties and may help close the bid-ask gap that has constrained resale volumes.

For investors holding ready secondary-market assets, the improving mortgage environment is a material tailwind: more mortgage-eligible end-users means more potential buyers for your exit, which supports valuations. If you are considering financing a Dubai property purchase yourself, the expat mortgage guide covers current lending criteria, LTV ratios, and the step-by-step application process.

Area-by-Area Price Per Square Foot Guide — Q1 2026

One of the most useful outputs from Q1 2026 data is a comprehensive price-per-square-foot landscape. The variance across Dubai is now extraordinary:

| Area | Price per sqft (AED) | Segment |

|---|---|---|

| Emirates Hills (villas) | ~14,500 | Ultra-luxury |

| Palm Jumeirah (villas) | 12,000–16,000 | Premium |

| Downtown Dubai (apartments) | 2,450 | Premium |

| Off-plan apartments (market avg) | 2,100 | New-build |

| Secondary villas (market avg) | 2,354 | Resale |

| Dubai Marina (apartments) | 2,061 | Mid-premium |

| Jumeirah Village Circle | 1,050 | Affordable |

| Dubai South | 900–1,400 | Growth corridor |

Emirates Hills villas at AED 14,500 per square foot versus Dubai South apartments at AED 900 represents a 16x variance across the same city. That spread is not irrational — it reflects access to amenity, community prestige, infrastructure quality, and capital permanence. But it does mean that “Dubai real estate” as a single investment thesis is dangerously imprecise. The right question is never simply whether to invest in Dubai. It is where within Dubai, at what price point, and for what hold period and exit strategy.

What Q1 2026 Means for Buyers and Investors Right Now

The data consolidates into clear strategic signals depending on where you sit in the market:

Villa buyers remain in a structurally supported market. Supply in established communities is constrained, end-user demand is strong, and appreciation has been consistent across almost all villa submarkets. The caution: avoid overpaying at cycle peaks for ultra-luxury assets where yields are already compressed. The opportunity: emerging villa communities — Damac Hills, Town Square, Dubai Hills Estate — that have not yet fully repriced to match golden triangle premiums.

Apartment investors must exercise location discipline. The top quartile of apartment communities by location quality continue to deliver meaningful appreciation. The bottom half will face competition from substantial new supply completing through 2026 and 2027. Buying a well-located apartment is entirely defensible; buying the cheapest available unit in a peripheral community is speculative at current prices.

Mortgage buyers are entering a more favourable rate environment. As borrowing costs decline and the qualifying buyer pool expands, end-user demand strengthens — benefiting both the purchase and future resale of mortgage-bought properties.

Golden triangle buyers should understand they are acquiring wealth preservation assets, not yield instruments. Capital appreciation in Palm Jumeirah, Emirates Hills, and MBR City has been historically robust. But entry at current averages — AED 44.6 million for Palm Jumeirah villas — compresses running yields significantly. The investment case rests on long-term capital growth and Dubai’s continuing appeal as a global wealth hub, not on rental income.

For a broader framework on why Dubai continues to outperform comparable global markets over the long term, read our comparison of Dubai vs London, Singapore, and New York.

Looking Ahead: The Signals to Watch in Q2 2026

Several forces will shape whether the Dubai property market Q1 2026 momentum carries into the second quarter and beyond.

New supply deliveries. Approximately 60,000 units are scheduled for handover across 2026 — the majority apartments in emerging communities. Absorption rates will be the key metric. If the market digests new supply without significant price softening, the structural demand thesis is confirmed. If vacancy rates rise in peripheral communities, the apartment bifurcation will intensify.

Interest rate trajectory. Further Fed cuts feed through to UAE mortgage rates and have an outsized effect on the end-user buyer pool. Each 25 basis point reduction meaningfully improves affordability and expands demand.

Geopolitical safe-haven flows. Dubai continues to attract capital seeking a politically stable, tax-efficient domicile. As long as global uncertainty persists, that positioning advantage remains. The data from Q1 — particularly in the golden triangle — reflects exactly this dynamic.

Regulatory evolution. Dubai’s DLD and RERA have maintained transparent, buyer-protective frameworks. Any evolution of escrow rules, SPA protections, or project completion guarantees would affect off-plan demand directly. The direction of travel has historically been toward greater buyer protection, which supports confidence.

The Bottom Line

The Dubai property market Q1 2026 data tells a story that headline aggregates cannot. Forty-seven thousand transactions worth AED 176.7 billion confirm that the market is large, liquid, and growing. The 35% villa surge versus 3% apartment growth tells you where momentum is concentrated. The 46% mortgage value increase signals that end-user demand is broadening and financing conditions are improving. And the golden triangle’s concentration of premium capital tells you that the world’s wealthiest buyers are making long-term commitments to specific Dubai postcodes.

Read the data carefully. It tells you not just where the market has been — it tells you where to position next.